How Reforming Stock Market Rules Would Dramatically Boost America’s Middle Class

Just imagine how much it would help the middle class to enjoy access to America’s wealth engines again.

Just imagine how much it would help the middle class to enjoy access to America’s wealth engines again.Investors are always looking for hot stocks. But what if the hottest stocks became that way via cursed baptism in a certain lake of fire?

Sulfur and brimstone are two commodities not many should be excited about adding to their portfolio. And yet the world of investing has a twisted fascination with companies that deal in vice. There’s one particular mutual fund that singles out investments in “sin stocks” like cannabis and casinos. The investment thesis is that buying into morally murky industries is a long-term win because addicts make loyal customers, and even in bad economies, people still want to get high.

If people are serious about making America great again, they must consider what their investments are funding.

But the Vice Fund is not actually all that unique — it is just saying the quiet part out loud.

There are hundreds of mutual funds and ETFs invested in the shady businesses of abortion drugs, pornography, strip clubs, and LGBT activism. But what you might not realize is that there is a good chance you own one of those funds in your 401(k), IRA, or other investment fund.

Don’t believe me? Type one of your ticker symbols into www.inspireinsight.com and see for yourself.

It's easy to be deceived. These dirty funds have normal-sounding names from reputable companies like American Funds Growth Fund of America, iShares Core S&P 500 ETF, and Vanguard Large Cap Index Fund. The devil comes disguised as an angel of light, after all.

But don’t be too hard on yourself. If anyone should have known better it was me. I had the wool pulled over my eyes, too. A financial adviser working in the lofty private client group of a prestigious bank and a dedicated pro-life Christian, I was dumbfounded the day I discovered that I was personally invested in three abortion drug manufacturing companies.

The unsettling truth pierced my heart that every time a young lady went to Planned Parenthood and had an abortion, I made money on that transaction. I literally profited from the murder of an innocent child and was recommending all of my wealthy clients to do the same.

But it didn’t stop there: porn, LGBT activism, human trafficking, the list went on like a “hottest stock picks” newsletter from hell. How could this be?

According to a recent study by the faith-based investing organization Kingdom Advisors, $22.4 trillion of investment assets are owned by Christian church members in the United States, representing about 50% of the entire investment market.

I have two questions: How much of that money is invested right now in industries and activities that are diametrically opposed to the biblical values their Christian owners seek to live their lives by? And how different might corporate America be — and indeed our nation at large — if those Christian investors directed their capital away from the works of evil and into companies that did good instead?

What if major corporations got the message that 50% of the investment assets in America were off limits to any business that manufactured abortion drugs? Or pushed LGBT activist agendas? Or distributed porn?

What if the mutual fund, ETF, and 401(k) providers got the message that 50% of the investment assets in America refused to invest in funds that bought morally compromised stocks?

RELATED: How corporate America helped fuel the hate that killed Charlie Kirk

I believe things would be much different — and much better. Last month, Costco announced its decision not to sell the abortion drug mifepristone in any of its pharmacies. This decision is a huge pro-life victory and followed a sustained shareholder engagement campaign that began more than two years before by my faith-based investing firm, Inspire Investing.

Thanks to Biden-era shenanigans, in 2023, long-standing safety restrictions limiting mifepristone distribution were loosened to allow retail pharmacies to apply for a special exemption to dispense the abortion pill directly: a dangerous practice that the U.S. Food and Drug Administration itself says puts women in elevated danger of hospitalization and potentially deadly complications, regardless of what you believe about abortion and the effect on the baby.

In early 2024, CVS and Walgreens jumped on the abortion bandwagon and signed up for the exemption. Other large retail pharmacies such as Costco, Walmart, Albertsons, and Kroger, were considering following suit. That's when our team snapped into action.

We leveraged our position as investors to lobby the investor relations department and made the strong case against getting into the abortion business. We gathered over 9,000 signatures from Costco members and investors ready to cancel their memberships if Costco started stocking mifepristone. We rallied a coalition, including faith-based investors, treasurers, and other financial officers from conservative states. We had numerous conversations with Costco’s management.

Liberal abortion activists were also hard at work, bringing their own firepower to bear.

In the end, goodness and common sense prevailed, and Costco made the rational decision to stay out of such a contentious and legally tenuous line of business, while also citing a “lack of demand from our members and other patients.” But it wasn't only Costco. Walmart made the same decision, and we are hopeful that other pharmacies will be listening to reason as well.

This isn't an isolated incident. You can read many more stories of the successes we’ve had, including details of the behind-the-scenes conversations influencing major corporations with conservative, biblical values in my book "Biblically Responsible Investing: On Wall Street as It Is in Heaven."

If people are serious about making America great again, they must consider what their investments are funding. Is your own money working against you?

Will you invest the hell out of your money?

Corporate America must answer for its part in the assassination of Charlie Kirk.

Years of platforming and promotion of the woke cancers of trans ideology, critical race theory, cultural Marxism, abortion, and many others through America’s largest corporations have done more damage than many realize. Cases like Bud Light and Target illustrate the harm companies have done to themselves by embracing these ideas. But also consider the damage they have done not just to their brands, but to society.

The cultural battle we are fighting is not just right versus left — it is good versus evil.

How might the world be different if instead of promoting LGBT propaganda in their storefronts and advertising, big businesses promoted traditional marriage and family values?

What if companies ditched mandatory trainings on “gender-affirming HR policy” and instead celebrated men of integrity and women of honor uniting in holy marriages and giving birth to lots and lots of children?

What if companies redirected the millions of dollars they donate to the abortion mafia every year toward Christian adoption agencies and pro-life clinics?

What if companies rewarded hard work and merit instead of skin color and sexual preferences?

That world is such a far cry from where we are today that it seems almost unimaginable. It underscores just how insidious is the cultural impact our corporations have had on American society.

A single crack of an assassin’s rifle shattered any remaining illusions about the moment we are in right now in our nation. Charlie Kirk’s martyrdom was the first to be witnessed by tens of millions of people around planet earth. The ensuing revival has been stunning and inspiring. The ghoulish celebration by those with darkened spirits has been disgusting.

Such contrast surrounding the atrocity of Charlie’s murder has put into sharp focus for me that the cultural battle we are fighting is not just right versus left — it is good versus evil. Medusa has taken off her hat and we can see the naked evil for what it is: hatred, pure and simple.

I only spoke with Charlie once. I was a big fan of his work. As I have reflected on the truly miraculous work he accomplished to activate the youth of our country toward conservative, Christian political engagement — a feat many told him was hopeless — I am put to shame that we have not done more in our sphere of influence among Christian investors to combat the evil emanating from the stocks in our portfolios.

According to Kingdom Advisor’s 2025 Report on the Christian financial industry, Christian church members in the United States own $22.4 trillion of investment assets, or roughly 49.7% of all investments in this country. That means 49.7% of all the votes for board members who appoint CEOs, set major corporate policy, and direct the corporation’s engagement on cultural issues.

If Christians have that sort of influence, why do the boardrooms of corporate America so often resound with anti-Christian sentiment?

RELATED: Prove Charlie right

It pains me to say that it is because these assets have been, in large measure, handed over to leftist corporations, mutual fund companies, and financial advisory firms to do with them what they will.

We as Christians, and conservatives more broadly, have given our power, influence, wealth, and shareholder votes to the enemies of our way of life. This must change.

The leftist ideology spewed by many corporate institutions and that animates the murderous hatred of Charlie Kirk is not simply a political viewpoint; it is an evil. Like all lies, it cannot stand before the truth. And like all darkness, it cannot stand against the light. But it howls and gnashes its teeth all the same.

Will we stand idly by as the demons run wild with our money? Or will we take back our wealth, influence, and shareholder votes from the big Wall Street firms and make sure our dollars are advocating for biblical values?

Together we can speak $22.4 trillion of biblical truth to corporate power — and there is no telling what God will do with that.

One of the late comedian George Carlin’s most famous rants gave us the line, "It's a big club ... and you ain't in it.” That sentiment rings especially true when it comes to the financial services industry, where wealthy investors and insiders gatekeep the most lucrative opportunities for themselves and their friends.

So what should you think when they suddenly want to let you in?

The private equity party is a bit dim right now, and that’s why they are sending out more invitations. Be careful before you RSVP.

There's no red flag bigger than when someone wants to let you in on something very exclusive — especially if it’s from people who’ve spent decades keeping you out of the club.

Case in point: the private equity industry’s latest push to open its funds to everyday retail investors.

The private equity world is one I know well, as a recovering investment banker who works with a firm to evaluate deals. My husband also worked in the sector. Like any other industry, it has both good and bad players.

Private equity involves deploying capital to buy ownership stakes in private companies, distinct from equity invested through the public markets in publicly traded companies. These firms are often actively involved with the company, as opposed to the more passive investing in public market companies. Their stakes are typically substantial, often including majority ownership.

The good players in private equity provide capital, professionalization of businesses, governance, business insights, and capital for growth. They may reward employees with an ownership stake to align incentives.

Some private equity players, however, focus on financialization — that is, playing around with the capital structure of a company and not adding a lot of value otherwise. Private equity is rife with examples of firms that have ruined businesses with too much leverage and engaged in a variety of greedy — and often, outright abhorrent — behaviors.

But this latest trend isn’t about good firms versus bad firms. It’s about the broader industry’s poor performance — and desperation.

Private equity has a problem. Too much money has flooded the space in recent years, driving up valuations and pushing down returns. Funds are struggling to find new investors to cover their high management fees. So now they’re turning to you.

They aren’t suddenly being generous. They’re just trying to survive.

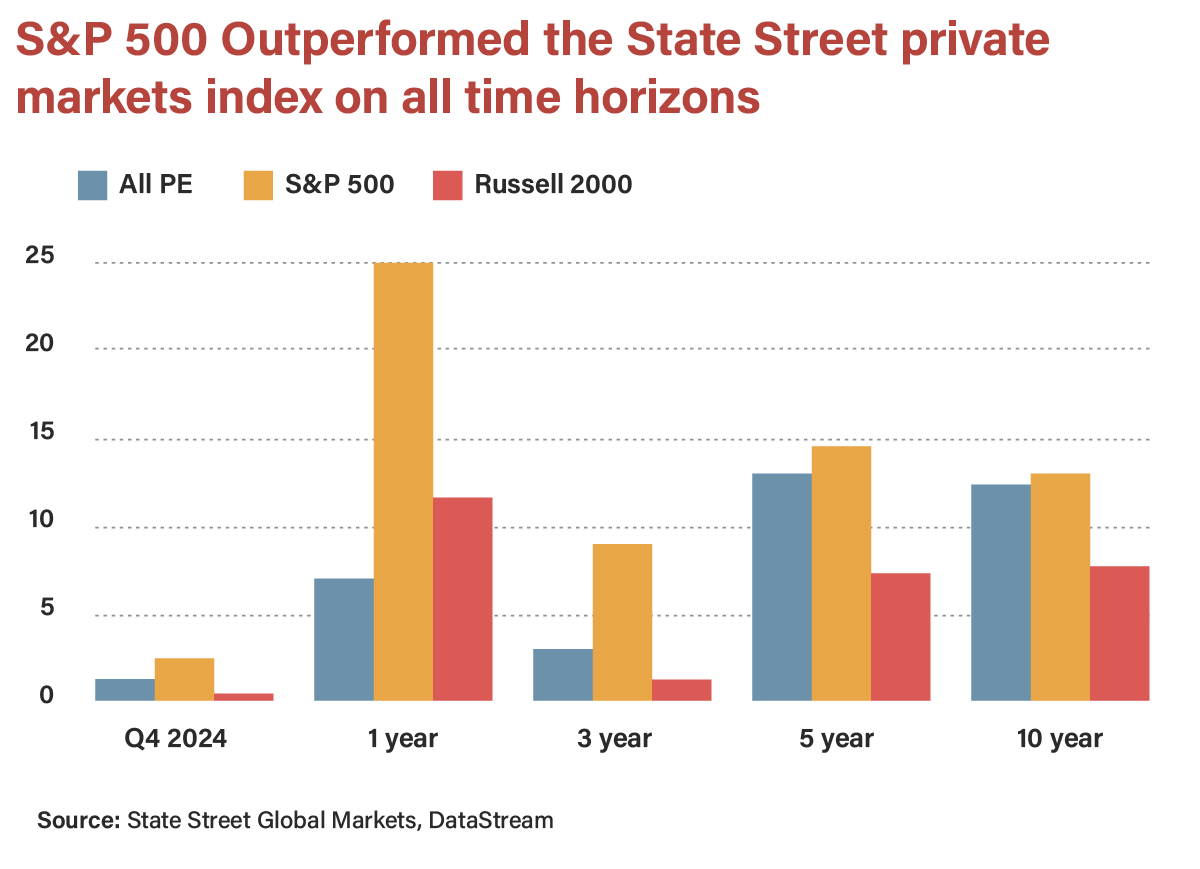

According to the Financial Times, a major private market index has underperformed the S&P 500 over the past one-, three-, five-, and 10-year periods. Any outperformance was skewed toward earlier years — and even then, it came with significantly higher fees and far less liquidity.

This underperformance comes with heavy fees and a lack of liquidity for your investment. It's not a coincidence that you are seeing private equity opening up to retail now when it is struggling from deal competition, higher valuations, higher capital costs, and slower deal exits.

RELATED: Red states get it: Economic freedom beats blue-state gimmicks

Speaking of slower exits, the Wall Street Journal noted that “private equity remains the biggest fee generator for the broader Wall Street ecosystem of banks and advisers” and that private equity firms are sitting on a record number of companies that they are waiting to exit — that is, sell and record a profit ... or a loss. Longer hold times for private equity firms mean they are not returning capital to their investors, and, in turn, the investors are not reinvesting in the latest and greatest fund.

Whether it’s the new push to allow private investments into your 401(k) or your financial planner calling you with “new, exciting alternative investment opportunities,” please be appropriately skeptical. Always probe a fund’s track record (especially over the past several years), fee structure, and whether it is a fit for your objectives and goals.

The private equity party is a bit dim right now, and that’s why they are sending out more invitations. Be careful before you RSVP.

Just weeks into President Donald Trump's second term, the S&P 500 — which had risen over 20% in the previous two years — rocketed to record highs, driven up in part by a substantive increase in corporate earnings as well as the "Trump bump."

After marking its all-time high of 6,144.15 on Feb. 19, the index soon began to slide, prompting anxiety among some investors and doom-saying from various analysts, especially over the potential impact of the president's tariff proposals.

For instance, Andrew Brenner, head of international fixed income at National Alliance Securities, told the New York Times a month ahead of Trump's "Liberation Day" tariff announcements, "The tariff rhetoric has become daily and extreme, sentiment is awful and trading is on edge."

In the days immediately following Trump's April 2 announcements, the S&P 500 had its worst day since COVID-19 crashed the economy in 2020, then shed many trillions in market value, prompting more of the concerns and shirt-rending that would become customary over subsequent weeks.

After months of doom and gloom, the S&P 500 hit a new record on Friday, marking a stunning comeback from April. At market open, the S&P 500 went north of 6,154.79.

CNBC suggested that the comeback — what Bloomberg indicated is "shooting toward the second-biggest percentage-point recovery in history" — was driven in part by strong corporate earnings, a stable labor market, and new energy in the AI trade. It certainly doesn't hurt that trepidation over tariffs has largely given way to optimism over Trump's trade deals.

The possibility that Trump might not ultimately implement his Liberation Day tariffs may also have been factored into investors' optimism. After all, the rise came on the heels of White House press secretary Karoline Leavitt noting that Trump's July tariff deal deadline "is not critical" and "could be extended."

There's also the matter of Commerce Secretary Howard Lutnick's recent revelations to Bloomberg News that the U.S. and China finalized its trade deal this week and that the Trump administration has imminent plans to reach trade deals with 10 other major trading partners.

"We're going to do top 10 deals, put them in the right category, and then these other countries will fit behind," said Lutnick.

RELATED: Trump’s tariffs take a flamethrower to the free trade lie

"The markets are looking forward, seeing lower interest rates, less regulation in the banking sector, a shift from austerity to stimulus in Europe, and a less biting inflation and tariff environment," Jamie Cox, managing partner at Harris Financial Group, told CNBC. "This sure isn’t the stagflation story we've been told to brace for."

Paul Stanley, chief investment officer at Granite Bay Wealth Management, said to CNN regarding the S&P 500's $9.8 trillion roundtrip, "The market is betting on continued progress on trade and a de-escalation of tensions in the Middle East is giving investors confidence."

Entrepreneur and business expert Carol Roth told Blaze News that "it's important to remember that the market is not the economy, and that other factors, including the Federal Reserve and government policy, have impacted the market, particularly over the last couple of decades."

"The president's heavy-handed approach to tariffs was not expected by the market, but as there had been more certainty gained regarding tariff policy and a belief that further de-escalation is more likely than escalation, the market has moved past that hurdle," explained Roth. "In recent days, commentary from Fed members that suggests a Fed rate cut may be on the table for July has supported risk assets."

Roth noted, however, that "any long-tail effects from tariffs that show up later in the year, or challenges that arise from financing/refinancing our massive debt and deficit could shift the outlook and impact market returns."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

President Donald Trump warned in the lead-up to the 2020 election that the stock market would crash in the event that Joe Biden and Kamala Harris were afforded an opportunity to lead the nation. When the crash did not come immediately, the liberal media laughed off his warning as politically charged nonsense.

Again, earlier this year, Trump warned that the market would be headed for trouble under the Harris-Biden administration, and again he was mocked like the Cassandra of Greek legend.

Sam Stovall, chief investment strategist at CFRA Research, was among the many who shrugged off Trump's doomsaying, telling CNN, "Fear sells."

The X account for what is now the Harris campaign shared a post in May mocking Trump's warning. President Joe Biden re-shared the post along with a meme insinuating Trump was a loser.

Months later, it became clear that Trump's fears, though premature, were justified.

A dismal Labor Department job report landed Friday, fueling fears of a coming recession and sparking a market selloff. Amid the U.S. market nosedive Friday, Trump responded on Truth Social, writing, "Kamalanomics."

'Of course there is a massive market downturn. Kamala is even worse than Crooked Joe.'

Markets tanked again Monday morning. Blaze News noted that the Dow opened down more than 1,000 points and as of mid-morning hovered about -2.6% overall. The tech-heavy Nasdaq, meanwhile, was down over 560 points or 3.36%.

The Chicago Board Options Exchange's Volatility Index (VIX), which reflects the market's expectations for the relative strength of near-term price changes of the S&P 500 Index, has shot up 170% since Friday and is poised for its biggest single day rise on record, according to Reuters.

Trump spared no time swapping out his warnings for blame.

"STOCK MARKETS ARE CRASHING, JOB NUMBERS ARE TERRIBLE, WE ARE HEADING TO WORLD WAR III, AND WE HAVE TWO OF THE MOST INCOMPETENT 'LEADERS' IN HISTORY. THIS IS NOT GOOD!!!" Trump wrote on Truth Social.

Trump later wrote, "Of course there is a massive market downturn. Kamala is even worse than Crooked Joe. Markets will NEVER accept the Radical Left Lunatic that DESTROYED San Francisco and California, as a whole. Next move, THE GREAT DEPRESSION OF 2024! You can’t play games with MARKETS. KAMALA CRASH!!!"

Having clearly settled on the alliterative put-down, Trump again took to Truth Social, writing, "VOTERS HAVE A CHOICE — TRUMP PROSPERITY, OR THE KAMALA CRASH & GREAT DEPRESSION OF 2024, NOT TO MENTION THE PROBABILITY OF WORLD WAR lll IF THESE VERY STUPID PEOPLE REMAIN IN OFFICE. REMEMBER, TRUMP WAS RIGHT ABOUT EVERYTHING!!!"

Trump's running mate, Sen. JD Vance (R-Ohio), took to X to note that this "moment could set off a real economic calamity around the globe. It requires steady leadership — the kind President Trump delivered for four years. Kamala Harris is too afraid to answer media questions and cannot lead us in these troubled times."

Rather than acknowledge the market bloodbath, the Democratic Party elected instead to celebrate Harris' record Monday, lauding her and her former running mate for "one of the greatest economic comebacks of any administration."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

The 1792 Exchange, a corporate bias watchdog seeking to restore political neutrality in the boardroom and to altogether combat woke capital, has released another damning batch of insights into the extent of the ideological capture at America's Fortune 10 companies.

The watchdog's recent analysis — critical additions to a growing database that tracks the political preferences of board members and leaders inside Fortune 250 companies' C-suites — indicates that executives from America's top 10 companies, taken in aggregate, direct the super-majority of their political giving to Democrats. The 1792 Exchange further highlighted various public remarks suggestive of executives' prioritization of left-wing activism in the name of so-called stakeholders over results and returns for those shareholders who have everything on the line.

The 1792 Exchange indicated that executives from Fortune 10 companies give 77% of their political donations to Democrats and only 23% to Republicans. The political bias is especially clear at Amazon, Apple, and Alphabet, where the ratio of political giving to Democrats over Republicans apparently exceeds 9:1. Of the three corporate behemoths, 97%, 97%, and 95% of political donations went to Democrats, respectively.

Two outliers among the Fortune 10 in this regard are Chevron and Walmart, where 81% and 69% of political donations from executives and board members went to Republicans.

Matt Buckham, vice president for programs at the 1792 Exchange, told Blaze News, "What we see is instead of having a fair representation of viewpoints, instead of having a clear understanding that we are serving the shareholder, we see a massive tilt of 'We favor one party’s political opinions, one party’s ideas, one party’s ideology.'"

Buckham suggested that these executives should alternatively be focused on the business — on "doing what's good for the shareholder, what's good for the customer, and making the best product or service possible. Activism is the complete opposite of that."

"We don't want them to take harmful, left-wing, Democratic activist viewpoints and ideologies and incorporate them in a business with the pretense that it's helping the shareholders," continued Buckham. "We're trying to help companies avoid another Bud Light moment."

In an apparent effort to signal its woke alignment, Bud Light collaborated last year with transvestite influencer Dylan Mulvaney, celebrating his supposed "365 Days of Girlhood." The leftist activism hurt the company and shareholders by extension.

A boycott reacting to the company's apparent mockery of women successfully took Bud Light out of the ranking of America's list of top 10 beers, cost Anheuser-Busch tens of billions in market value, and prompted a purge of corporate employees. According to the Harvard Business Review, Bud Light's sales decline persisted for around eight months.

It is unclear whether the executives at America's Fortune 10 companies — Walmart, Amazon, ExxonMobil, Apple, UnitedHealth Group, CVS, Berkshire Hathaway, Alphabet, McKesson, and Chevron — have taken the Bud Light lesson to heart. It is clear, however, that many are predisposed to a potentially costly leftward drift.

Referencing public statements made by company directors in recent months and years, the 1792 Exchange report indicated that ESG and DEI are baked into executives' conversations and considerations.

The report highlighted, for instance, former PepsiCo. CEO and current Amazon Audit Committee chairman Indra Nooyi's sense that discriminatory hiring policies are the way forward.

"You have to put some quotas and numbers in place to get the appropriate critical mass of diverse people in," Nooyi is quoted as saying at a 2022 leadership event in Dubai. "Don't look at quotas as something bad. It's bad if it's not in the early stages. So if it's in the early stages, start with a quota. Insist that the numbers get to 25[-]30% diverse people."

"[Inclusion] starts with numbers and then becomes a mindset," continued Nooyi.

Nooyi is evidently not the only race obsessive with priorities besides profitability at Amazon.

Andy Jassy, the company's president and CEO, reportedly said, "If you knew what a lot of the senior leaders at Amazon spend their time on when they're not at work. They spend their time on issues of racial equality. People are very passionate about it. I spend a lot of my time on that, too, so I care a lot about it."

It appears even the directors at ExxonMobil have waved on the leftist march through corporate institutions.

The 1792 Exchange highlighted how Gregory Goff, an independent director at the oil giant since 2021, is among those who have bought into stakeholder capitalism contra shareholder capitalism.

"I would hope that a director or directors would never compromise those plans and [ESG] programs by maybe challenging how much money is being spent on the things that are the most important to do," said Goff.

Things are no better at the UnitedHealth Group where the company's so-called chief innovation officer Dame Vivian Hunt appears to be of the mindset that the company must embrace an activist role. Huntnoted at an Imperial College Business School conference, "We want to lead responsibly. Stakeholder capitalism is a framework to do so. It's new harmony with a brain, a balance sheet, as well as a heart."

Over at Google's parent company Alphabet, board member Roger Ferguson Jr., is apparently of the mind that capitalism is broken and needs to be fixed.

"Business leaders must embrace a new definition of capitalism that puts a greater emphasis on social responsibility and equity," Ferguson said at a 2021 gala where he was being honored. "The Business Roundtable took meaningful steps toward that goal when it redefined the purpose of the corporation to include a commitment to all stakeholders."

Paul Tice, an adjunct professor of finance at the Leonard N. Stern School of Business at New York University, indicated in his recent book, "The Race to Zero: How ESG Investing Will Crater the Global Financial System," that stakeholder capitalism theory, which began making the rounds in management circles around the 1960s, "argues that modern enterprises must serve not only shareholders but all company stakeholders — including employees, suppliers, and customers as well as the state, the economy, and society at large."

Tice suggested that stakeholder capitalism, particularly the kind championed by Klaus Schwab of the World Economic Forum, is built upon a corporatism "doubtless influenced by an engineering flow-chart mindset and a Prussian need to order society" that is "basically a collectivist political ideology with a dark lineage."

Buckham told Blaze News, "There's no end to what a stakeholder is or who a stakeholder is, so anybody and everybody can be one, they're loud."

"We're just saying [to company executives], 'Stop listening to everybody. Focus on your company — on what you do well, who you actually serve as the shareholder — and your company will do well," continued Buckham.

Just as Consumers' Research provides consumers with insights into how they can avoid giving woke companies their hard-earned cash, the 1792 Exchange — named in tribute to the founding of the first American stock exchange in 1792 — seeks to both chasten top executives and help investors "make sure that they know what's going on in the companies they're invested in."

Buckham indicated that the 1792 Exchange will keep furnishing investors with insights so they can avoid woke companies and have a hand in turning things around for the better.

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

These days, a million-dollar 401(k) doesn’t guarantee a cushy retirement.

These days, a million-dollar 401(k) doesn’t guarantee a cushy retirement.