How Reforming Stock Market Rules Would Dramatically Boost America’s Middle Class

Just imagine how much it would help the middle class to enjoy access to America’s wealth engines again.

Just imagine how much it would help the middle class to enjoy access to America’s wealth engines again.Most Americans assume that if their deposits are insured, their banking relationship is stable.

For decades, that assumption has been reasonable. Large national banks offer scale, convenience, and integration across checking, credit cards, mortgages, investments, and digital tools. For many households and businesses, they remain the default choice — for many good reasons.

Regional and community banks typically face fewer reputational signaling incentives and fewer reasons to police customers’ lawful beliefs.

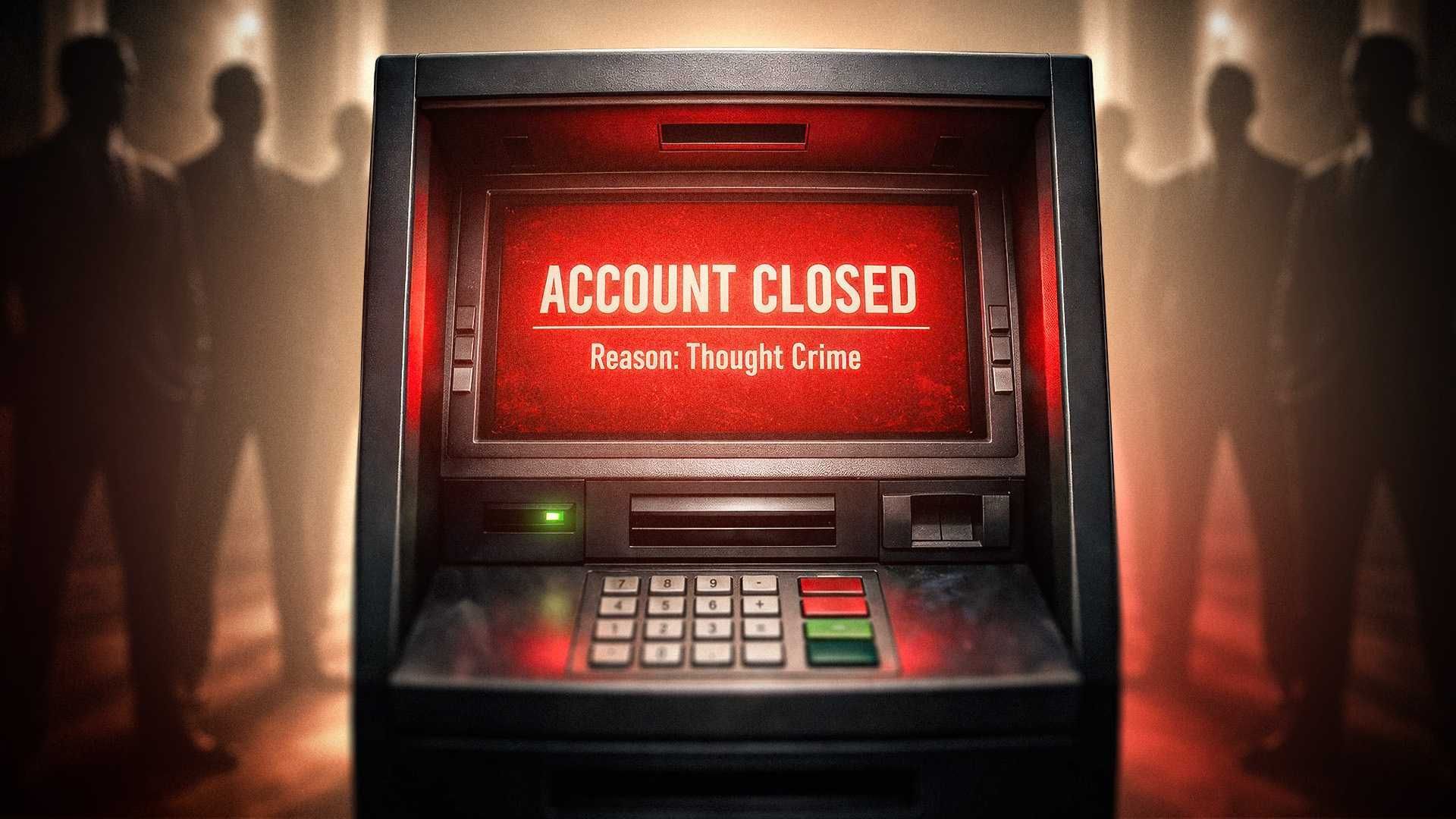

But in recent years, some lawful customers have found accounts restricted or closed not for fraud or criminal conduct, but because the financial institution decided internally that the customer is a risk to the institution's reputation or political standing. In other words: They have been canceled.

These cases are often hard to prove — and that difficulty is itself the problem. First lady Melania Trump revealed in her memoir that a bank decided to "terminate" her account. The reasoning was frustrating to pin down, since decisions on account restrictions are shielded from public verification by opaque risk explanations and confidentiality rules.

Other cases were clearer. In 2023, internal documents revealed that U.K. private bank Coutts closed the account of British politician Nigel Farage after deciding his political views posed “reputational risk” — a disclosure that ultimately led to the resignation of National Westminster Bank's chief executive.

“If they can do it to me, they can do it to you, too,” Farage proclaimed after the dispute.

Your money may be insured, but access to it is governed by institutional judgment. For some consumers, understanding where that judgment lies is now part of responsible financial planning.

That’s where this guide comes in. It’s not a broadside against megabanks. It is a road map for readers who want to understand the trade-offs that come with scale — particularly when account access is governed by broad, centralized risk frameworks rather than personal relationships or clearly defined misconduct.

Regulators have since moved to clarify standards governing account closures and risk assessments. But for consumers who watched large institutions end financial relationships under ambiguous or shifting rules, the question remains straightforward: Why assume that risk if alternatives exist?

There are no guarantees. But there are differences — rooted in structure, incentives, and how close a branch is to customers — that can meaningfully affect how ideological risk is handled.

Ideological risk is not evenly distributed. It tends to correlate with scale, distance, and discretion, rather than with partisan labels.

This guide organizes banks into categories based on structure and incentives, not ideology.

All banks listed below meet the following baseline criteria:

They are often safer. Regional and community banks typically operate on relationship-based models, with decision-making closer to customers and local markets. They face less national activist pressure, fewer reputational signaling incentives, and fewer reasons to police customers’ lawful beliefs.

Here’s what to look for:

Warning: Not all community banks are equal. Some rely heavily on third-party compliance vendors or adopt national risk frameworks wholesale. Size alone is not a guarantee.

Here are some strong options.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.8 (32.2K reviews); Apple 4.8 (47K reviews)

Region/States: 730+ branches in 17 states

ATM: MoneyPass network

Woodforest National Bank is a privately owned, community-focused financial institution headquartered in The Woodlands, Texas, that has provided banking services since 1980, operating hundreds of branches across multiple states and offering products for both personal and business customers. It offers a full range of financial services including checking and savings accounts, loans, debit cards, online and mobile banking, and other products designed for everyday banking needs. The bank emphasizes customer relationships, convenient access — including retail locations and digital tools — and a commitment to serving the communities where its customers live and work.

FDIC-insured: Yes

Credit card: Yes (via Premier Bankcard)

App: Yes — Google 4.5 (1.48K reviews); Apple 4.4 (1.4K reviews)

Region/States: 13 branch locations in South Dakota

ATM: Fee-free access to 37,000+ MoneyPass ATMs nationwide

First Premier Bank is an independently owned, FDIC-insured community bank headquartered in Sioux Falls, South Dakota. It offers a full range of financial products and services, including personal, business, and agricultural checking and savings accounts, loans and mortgages, wealth management, and digital banking. The bank also operates Premier Bankcard, a nationally recognized issuer of Mastercard credit products. First Premier emphasizes strong capitalization, customer support, community investment, and accessible online and mobile banking tools for managing finances nationwide.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.7 (987 reviews); Apple 4.8 (9.7K reviews)

Region/States: 24 locations in Dallas-Fort Worth

ATM: ATMs at nearly all branches

American National Bank of Texas is a long-established, independently owned, FDIC-insured community bank headquartered in Terrell, Texas, with more than 30 branches serving North Texas. It offers a full suite of financial products and services including personal and business checking and savings, loans and mortgages, digital banking, and wealth management. The bank emphasizes local relationship-driven service, community involvement, and comprehensive financial solutions tailored to individuals and businesses alike.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.9 (15 reviews); Apple 4.6 (192 reviews)

Region/States: 18 locations in Iowa, South Dakota, Nebraska

Liberty National Bank (Midwest) is an independently owned, FDIC-insured community bank headquartered in Sioux City, Iowa, founded in 2003. With approximately $600 million in assets, it serves customers across Iowa, South Dakota, and Nebraska, including Sioux City, Sioux Falls, and surrounding communities. The bank emphasizes local decision-making, relationship-based service, and support for families, businesses, and agricultural clients in the markets it serves.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.5; Apple 4.9

Region/States: ~10 locations in Oklahoma and North Texas

ATM: 20 local ATMs

Liberty National Bank (Texas/Oklahoma) is an independently chartered, FDIC-insured community bank headquartered in Lawton, Oklahoma. Originally established in 1902 as the Bank of Elgin, it adopted the Liberty National name in 2002 and has since expanded across Oklahoma and into North Texas, with assets exceeding $1 billion. The bank remains under Green family ownership and emphasizes long-standing ties to local communities, regional growth, and personalized banking relationships.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.6 (322 reviews); Apple 4.8 (1.1K reviews)

Region/States: 33 locations in California

ATM: Pulse & Cirrus (400,000 ATMs)

Farmers & Merchants Bank of Central California offers personal and business banking services, including a variety of checking and savings accounts, loans, and agricultural financing tailored to individuals and companies across numerous California communities. The website emphasizes secure 24/7 online and mobile banking so that customers can manage accounts, transfer funds, pay bills, and access eStatements from anywhere. It also highlights local branch access, community roots dating back over a century, and a commitment to serving customers’ financial needs.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 2.8 (82 reviews); Apple 4.6 (790 reviews)

Region/States: 18 locations in Virginia, West Virginia, Tennessee, North Carolina

ATM: Allpoint (55,000 locations)

New Peoples Bank is a community-focused financial institution with multiple branches serving individuals and small to medium-size businesses across Southwestern Virginia, Southern West Virginia, Northeastern Tennessee, and Western North Carolina, offering a full suite of personal and business banking products including checking, savings, loans, and online services. Through its website, customers can open accounts, apply for mortgage or personal loans, manage finances with online and mobile banking tools, and access additional services like identity protection and ATM networks. The bank emphasizes local decision-making, Golden Rule customer service, and technology that supports secure, convenient banking experiences.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 3.8 (51 reviews); Apple 4.8 (431 reviews)

Region/States: 7 locations in Kentucky

ATM: MoneyPass

First United Bank and Trust Company is a community-oriented, FDIC-insured bank offering a full range of personal and business financial services, including checking and savings accounts, loans, digital banking, and trust solutions accessible online or at local branches. The bank emphasizes convenient 24/7 access to accounts, tools for managing finances, and solutions like credit cards and business services tailored to local needs. Its website highlights personal service, community engagement, and products designed to support customers’ financial goals with trusted relationships and modern banking technology.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.4 (132 reviews); Apple 4.8 (399 reviews)

Region/States: 6 locations in Iowa and Nebraska

ATM: MoneyPass

Arbor Bank is a community FDIC-insured bank offering a wide range of personal and business financial products, including checking and savings accounts, online/mobile banking, lending solutions, and mortgage services. It also provides business banking tools like treasury management, SBA loans, and positive pay fraud protection, along with card solutions and insurance options. The website emphasizes secure digital access, personalized service, and support for customers’ financial growth.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 3.6 (82 reviews); Apple: 4.6 (1.5K reviews)

Region/States: Over 750 First Command Bank advisers in over 175 offices in 45 states and Guam

ATM: MoneyPass ATM network and NYCE network; reimburses non-FCB ATM surcharges up to $10 per statement cycle

First Command’s banking section highlights personal banking products tailored for military personnel, veterans, and their families, including competitive checking and savings accounts, CDs, car loans, and debt consolidation options. These services come with convenient online and mobile access so that customers can manage funds, pay bills, and transfer money securely from anywhere, backed by the FDIC-insured protection First Command Bank offers. The emphasis throughout is on helping service members and their families manage everyday finances and build solid financial habits.

FDIC-insured: Yes

Credit card: No (mobile app offers free credit report updates weekly)

App: Yes — Google: 4.7 (1.24K reviews); Apple: 4.8 (3.1K reviews)

Region/States: 19 locations in Florida (The Villages and surrounding counties)

ATM: On-site ATMs at most branch locations; part of the Publix Presto! ATM Network (1,300+ surcharge-free ATMs across the Southeast); additional access through regional shared ATM arrangements (fees may vary depending on network)

Citizens First Bank is an FDIC-insured community bank serving The Villages and surrounding counties in Florida. It offers personal and business checking and savings products, robust online and mobile tools including bill pay and eStatements, and an ATM network focused on surcharge-free access. The bank merged with Seacoast Bank in October 2025 following the acquisition of its parent company, with conversion of accounts tentatively scheduled for July 2026.

FDIC-insured: Yes

Credit card: No

App: No dedicated mobile app; online account management via EmigrantOnline®

Region/States: 2 locations in New York; 1 location in Miami, Florida

ATM: On-site ATMs at branch locations; The bank refers to participation in ATM networks, though specific network details and surcharge policies are not prominently disclosed on its website. Prospective customers should confirm ATM access and fee policies directly with the bank.

Emigrant Bank is a privately owned U.S. financial institution offering high-yield savings, checking accounts, CDs, and mortgage lending. It emphasizes competitive deposit products and online/telephone banking access rather than a large retail branch footprint. Emigrant also provides mortgage lending through its direct lending division and support for account holders with tools to handle funds and financial needs securely.

Credit unions are member-owned, less PR-sensitive, and historically focused on service rather than signaling. Because there are thousands of local credit unions with varying eligibility rules, this guide does not list specific institutions.

How to find a good one:

This is the smallest and most visible category — and the one that requires the most due diligence before joining.

The claim here is not that these banks are “conservative,” but that they have made explicit commitments to viewpoint neutrality and have no public record of ideological account closures.

What qualifies:

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.6 (940 reviews); Apple 4.8 (1.5K reviews)

Region/States: Nationwide digital access; one physical branch

ATM: MoneyPass (40,000+ ATMs)

Old Glory Bank is a full-service, FDIC-insured American bank headquartered in Elmore City, Oklahoma, offering personal and business checking and savings accounts, loans, certificates of deposit, and modern digital tools like mobile and online banking with nationwide access. It positions itself as a nationwide online bank built around traditional American values and strong commitments to privacy, security, and customer autonomy. Customers can bank digitally from all 50 states while also accessing features such as ATM networks, cash deposit options, and advanced debit card controls.

Co-founded by John Rich, Dr. Ben Carson, Larry Elder, and former Oklahoma Gov. Mary Fallin (R), Old Glory is guided by what it calls the Banking Bill of Rights. A statement to Align from the founders makes the bank’s stand against de-banking central to its mission: “Not only does Old Glory Bank have a policy on de-banking, it is the very reason we exist! We were founded in direct response to the growing and troubling practice of de-banking Americans for their lawful, constitutionally protected beliefs. We saw the alarming trend in January 2021 and got to work years before it became newsworthy. We stand firm on the belief that this practice is morally, legally, and fundamentally incompatible with the freedom upon which our nation was built.”

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.8 (21 reviews); Apple 4.9 (523 reviews)

Region/States: 7 locations in Oklahoma, Texas, Missouri

ATM: 10 free out-of-network transactions monthly

Regent Bank is a regional, FDIC-insured, full-service bank headquartered in Tulsa, Oklahoma, with multiple branches in Oklahoma, Texas, and Missouri, offering personal and business banking products including checking, savings, loans, digital banking, and treasury services. It emphasizes personalized, concierge-style service tailored to entrepreneurs, small and mid-market businesses, and specialized niches like health care, agriculture, and nonprofits. The bank combines traditional community banking values with modern tools and solutions, supporting clients’ financial needs through dedicated local relationships and digital access.

A Regent Bank spokesperson told Align that the institution identifies as a “Christian, faith-based organization in terms of [its] mission and values” and that its “approach is grounded in relationship-driven banking and serving clients based on lawful activity — not political or religious beliefs.” Regent’s spokesperson added that de-banking is a frequently discussed issue at the executive level of the organization.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.5 (128K reviews); Apple: 4.9 (521K reviews)

Region/States: 1,445 locations across 15 states spanning the South, Midwest, and Texas

ATM: No-fee access at Regions ATMs

Regions Bank is a large, FDIC-insured, full-service financial institution and subsidiary of Regions Financial Corporation, offering a broad range of personal banking products including checking and savings accounts, loans and mortgages, digital banking, and wealth management solutions. It serves millions of customers through an extensive branch and ATM network across the South, Midwest, and Texas, while also providing online and mobile tools for everyday account management The bank combines traditional community-oriented service with modern digital convenience to support a wide spectrum of consumer financial needs.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.6 (6.8K reviews); Apple: 4.7 (29K reviews)

Region/States: ~20 branches in Utah and other Western markets

ATM: No-fee ATM network serving Western U.S.

Zions Bank is a full-service, FDIC-insured regional bank operating as part of Zions Bancorporation, offering personal banking products such as checking and savings accounts, loans and mortgages, credit cards, and robust digital banking tools including online and mobile access. It serves individuals and small businesses through an extensive network of full-service branches across multiple Western states and emphasizes community-focused service with modern financial solutions. Founded in the 19th century and rooted in local market relationships, Zions Bank combines traditional banking values with convenient digital access for everyday financial management.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.7 (10.6K reviews); Apple: 4.8 (50K reviews)

Region/States: 40+ locations in Alabama and Georgia

ATM: Unlimited fee-free Pinnacle Financial Partners ATMs

Synovus is a large, FDIC-insured financial services company and bank holding company headquartered in Columbus, Georgia, offering a full range of commercial and personal banking products including checking and savings, loans, mortgages, credit cards, and digital banking. It also provides specialized services such as wealth management, trust and investment solutions, treasury management, and mortgage and capital markets services through its subsidiaries. Synovus operates an extensive branch and ATM network across the Southeast and emphasizes personalized client relationships alongside modern digital tools.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 3.6 (12.5K reviews); Apple: 4.9 (252K reviews)

Region/States: 310 locations in Arkansas, Kansas, Missouri, and Oklahoma

ATM: Offers ATMs with live teller drive-thru services

Arvest Bank is a regional full-service bank offering personal and business financial products including checking and savings accounts, loans and mortgages, credit cards, wealth and treasury management, and secure online and mobile banking tools. Through its extensive network of branches across Arkansas, Oklahoma, Missouri, and Kansas, the bank emphasizes local community commitment while providing modern digital conveniences like 24/7 account access and mobile deposits. Its mission centers on partnering with customers to deliver tailored financial solutions that support everyday banking needs and long-term financial goals.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.5 (1.3K reviews); Apple 4.9 (8.7K reviews)

Region/States: 55 branches across Texas, including Austin, Corpus Christi, Dallas, Fort Worth, Houston, Lubbock, San Antonio, and the Rio Grande Valley

ATM: Branch and regional network ATM access (confirm surcharge policies directly with bank)

Founded in 1988 in Lubbock, Texas, PlainsCapital Bank has grown into one of the largest independent banks in the state, with approximately $12.4 billion in assets and more than 1,000 employees. A subsidiary of Hilltop Holdings Inc., it operates a statewide branch network and offers commercial banking, treasury management, private banking, wealth management, and consumer banking services. While emphasizing relationship-based banking, PlainsCapital functions at the scale of a large regional institution with centralized infrastructure and enterprise-level risk management.

Not every “alternative” bank actually reduces ideological risk.

If ideological or reputational risk is a concern, you don’t need to announce your politics or interrogate your bank. You’re simply trying to understand process, discretion, and escalation — the same way you would with fees, fraud protection, or data security.

These are reasonable, neutral questions.

1. Under what circumstances can my account be restricted or closed?

Listen for clear references to fraud, illegality, or operational risk. Be cautious if you hear broad or undefined references to “reputational,” “social,” or “values-based” concerns.

2. Will I receive notice before an account is restricted or closed?

Ask:

Advance notice reduces risk regardless of ideology.

3. Is there an appeal or escalation process if a decision is made?

Important follow-ups:

The ability to appeal matters as much as the rule itself.

4. Who ultimately makes account-closure decisions?

You’re listening for local or relationship-based decision-making versus centralized compliance teams or third-party vendors. Distance often correlates with opacity.

5. Do you rely on third-party compliance or risk vendors?

This matters because:

6. How do you define “reputational risk”?

A strong answer ties reputational risk to concrete financial, legal, or operational exposure.

A weak answer uses vague or moralized language without boundaries.

7. Are account decisions based on lawful activity, regardless of belief or affiliation?

Banks that can say this plainly usually mean it.

8. Is my account subject to special monitoring or enhanced review?

This is especially relevant for nonprofits, small businesses, and public-facing individuals.

You don’t need perfect answers. You’re looking for a bank that can explain its rules clearly — and show how decisions are reviewed.

A former member of the Donald Trump administration is set to take over Meta as president and vice chairman.

The appointment means an official from the president's first administration will now be in charge of the massive social media platforms Facebook, Instagram, and Threads.

'She is a fantastic, and very talented, person, who served the Trump Administration with strength and distinction!'

Mark Zuckerberg's Meta announced on Monday that it has called on 52-year-old Dina Powell McCormick to take the lead at the company. Powell McCormick served as Trump's deputy national security adviser for strategy from March 2017 to January 2018.

Powell McCormick was married to Richard Powell, a public relations and communications executive, but is now married to Sen. Dave McCormick (R-Penn.). Powell McCormick's maiden name is Habib; she was born in Egypt and speaks Arabic.

RELATED: Microsoft CEO: AI 'slop' is good for you — or at least for your 'human potential'

Powell McCormick was once referred to as Trump's "Ms. Fix It," and according to The Hill, informally advised Ivanka Trump during the transition period for Trump's first term. She had previously worked as a senior White House adviser in the George W. Bush administration, was director of the White House Presidential Personnel Office from 2003 to 2005, and served as assistant secretary of state for educational and cultural affairs in mid-2007.

Powell McCormick worked for Goldman Sachs for 16 years as a partner in senior leadership roles, according to Variety, after which she became vice chair, president, and head of global client services at BDT & MSD Partners, a merchant bank.

In addition, Powell McCormick is a fellow at Harvard, where she served as a teacher at the John F. Kennedy School of Government.

RELATED: Meta accused of deleting scam ads to dodge government regulation

President Trump praised the executive's appointment in a post to Truth Social, calling Powell McCormick a "great choice" by Zuckerberg.

"She is a fantastic, and very talented, person, who served the Trump Administration with strength and distinction!" Trump wrote.

At the same time, Zuckerberg said the new president brings experience in finance, economic development, and government.

"She'll be involved in all of Meta's work, with a particular focus on partnering with governments and sovereigns to build, deploy, invest in, and finance Meta's AI and infrastructure," Zuckerberg said in a Facebook post.

The Facebook founder also said that he and Powell McCormick will "deliver personal superintelligence" that will benefit billions of people.

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

A challenger to traditional banking has finally emerged, and it is coming from the right wing.

After billionaire Palmer Luckey was reported to be starting a cryptocurrency venture, it was unclear how big the scope would be and if it would work only in digital currencies.

Now that public filings have emerged, the new project was revealed to have major conservative backing while literally giving traditional banks a run for their money.

'The bank will be a national bank ... providing traditional banking products.'

Blaze News reported last week that Luckey had teamed up with Joe Lonsdale to start the new company; Lonsdale co-founded Palantir Technologies with Luckey and has his own software companies, as well. At the same time, Lonsdale's venture firm 8VC led a $225 million fundraising round for the new company to meet federal regulatory requirements.

The tech entrepreneurs were first thought to be starting a bank that would work primarily on maximizing returns for tech startups, but recent filings revealed much more is in store. According to the Financial Times, the new company has applied for a national bank charter, which would it give license to operate as a typical banking institution.

The Times also revealed a new right-wing mega-donor has joined the mix.

RELATED: Palmer Luckey-led crypto bank promises startups a capital hoard safe from scheming feds

None other than Peter Thiel and his venture capital fund, the Founders Fund, will also be backing the startup, according to two of the Times' sources.

Thiel is, of course, known for giving millions to Republican campaigns over the years, including over a million dollars to President Donald Trump for his 2016 campaign.

This new undertaking, dubbed Erebor, is yet another one of Luckey's companies named after themes found in J.R.R. Tolkien books. This one refers to the mountain in "The Hobbit," where the dragon Smaug hoards his gold. His other companies, Anduril and Palantir, are references to a character's sword and a magical seeing stone, respectively.

Filings revealed, "The bank will be a national bank ... providing traditional banking products, as well as virtual currency-related products and services, for businesses and individuals."

Adding to previous speculation, the target market was listed as businesses that are part of the American "innovation economy," including tech companies focused on virtual currencies, artificial intelligence, or defense manufacturing.

RELATED: The One Big Beautiful Bill Act hides a big, ugly AI betrayal

Erebor will work with stablecoins, cryptocurrency tied to relatively stable assets like the U.S. dollar or gold. This is done to limit the volatility of a coin without sacrificing its benefits, creating investment opportunities far in excess of simply purchasing and holding, say, Bitcoin.

For example, President Trump works with the stablecoin USD1, which is attached to the U.S. dollar.

"Longtime crypto people know it's a fine line between being targeted by government and being co-opted by government," explained Blaze Media's James Poulos. "But it's hard to strike the right balance without risking the worst of both worlds — a crypto economy that regulators tolerate but can destroy or manipulate with the wave of a hand."

Poulos added that the most stable compromise naturally involves figures that Washington relies on in other high-tech industries, "however much freedom-loving 'maxis' wish that weren't the case."

"Regardless, it doesn't matter how perfect a balance the kingpins of crypto and banking might strike if Bitcoin (to take the biggest example) falls short of its potential as a peer-to-peer currency and becomes just another place for established wealth to accrue value," Poulos concluded.

Erebor's filing said it plans on working with non-U.S. companies that are "seeking access to the U.S. banking system," according to the filing, and said it would "differentiate itself" by working with customers who are not well served by "traditional or disruptive financial institutions."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Billionaire Palmer Luckey is dipping his toe into the financial sector with a banking venture focused on helping tech entrepreneurs.

The company is known as Erebor, yet another entry in Luckey's portfolio that follows the Thiel-world pattern of referencing lore from the tales of J.R.R. Tolkien. Just as Anduril is a reference to a character's sword, and Palantir to a magical seeing stone, Erebor refers to the mountain in "The Hobbit" where the dragon Smaug hoards his gold away from would-be slayers and thieves.

While the moniker is not final, according to the New York Post, the venture is serious in its ability to reshape banking forever.

Deliberate federal interference in the nascent crypto banking market provoked the very crisis the feds purported to solve.

Luckey is partnering with Joe Lonsdale, a venture capitalist who co-founded Palantir Technologies and other software companies. Together, they will help tech startups build their businesses instead of maximizing returns like a traditional bank, insiders told the Post.

The key difference is that Erebor will work with stablecoins, a type of cryptocurrency tied to relatively stable assets like the U.S. dollar or gold. This is done to limit the volatility of a coin without sacrificing its benefits, creating investment opportunities far in excess of simply purchasing and holding, say, Bitcoin.

Even the president is working with stablecoins, particularly USD1, which is attached to the U.S. dollar.

RELATED: Big Tech execs enlist in Army Reserve, citing 'patriotism' and cybersecurity

The Post reported that Erebor was born out of the collapse of Silicon Valley Bank in 2023, caused by a slew of management errors, "investment missteps, market volatility, and regulatory changes," according to Investopedia. The Biden administration ended up guaranteeing all deposits into SVB, despite the bank's ruin.

But as Castle Island founding partner Nic Carter explained last year, deliberate federal interference in the nascent crypto banking market provoked the very crisis the feds purported to solve. "Biden bank regulators made it impossible for banks serving a particular legal industry to operate," Carter wrote. "And in doing so, they actively caused the collapse of certain banks, namely Silvergate and Signature. These banks did not die by suicide but by murder. This remains a gigantic scandal, and no one has ever faced any responsibility for it."

It is unknown who else is involved with the launch of Erebor; it is still in its early stages and has no public start date. Luckey's representative did not immediately respond to Blaze News' request for information regarding founders or key development points.

In that regard, Lonsdale's venture firm 8VC has led a $225 million fundraising round, which will reportedly be used to meet federal regulatory requirements that are necessary for starting a bank, not for backing deposits.

Luckey is not expected to hold an executive role or be involved in day-to-day operations, but he would be adding "bank operator" to his laundry list of titles, which include defense contractor and handheld-gaming manufacturer.

RELATED: Who's stealing your data, the left or the right?

The tech titan has increasingly been involved in larger-than-life projects, including advanced technologies for U.S. military equipment. His open-to-debate style has caused him to become a darling of the Silicon Valley class, and his prominent criticisms of Facebook/Meta (he has since buried the hatchet with Mark Zuckerberg) have helped his image as a palatable billionaire, a dynamic with echoes of Mr. Burns and his one-time rival Arthur Fortune.

"Cryptocurrency is so powerful and investable because it's the most advanced tech ordinary Americans can use right now amongst themselves to create and grow wealth," said James Poulos, Blaze Media's editor at large.

"But it's still not clear how exactly to transition the U.S. from a dollar backed by American global, economic, and military dominance to one backed by computational power," he added. "While stablecoins weaken the ability of regular people to use Bitcoin free from government pressure and control, they strengthen the ability of Washington and Silicon Valley to transition the dollar stably away from the unsustainable 'money printer' model toward a dollar backed by energy itself, in the form of watts used to power compute. That's why a bank like Erebor is basically inevitable."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Jamie Dimon, CEO of JPMorgan Chase — one of the most powerful financial institutions on earth — issued a warning the other day. But it wasn’t about interest rates, crypto, or monetary policy.

Speaking at the Reagan National Defense Forum in California, Dimon pivoted from economic talking points to something far more urgent: the fragile state of America’s physical preparedness.

We are living in a moment of stunning fragility — culturally, economically, and militarily. It means we can no longer afford to confuse digital distractions with real resilience.

“We shouldn’t be stockpiling Bitcoin,” Dimon said. “We should be stockpiling guns, tanks, planes, drones, and rare earths. We know we need to do it. It’s not a mystery.”

He cited internal Pentagon assessments showing that if war were to break out in the South China Sea, the United States has only enough precision-guided missiles for seven days of sustained conflict.

Seven days — that’s the gap between deterrence and desperation.

This wasn’t a forecast about inflation or a hedge against market volatility. It was a blunt assessment from a man whose words typically move markets.

“America is the global hegemon,” Dimon continued, “and the free world wants us to be strong.” But he warned that Americans have been lulled into “a false sense of security,” made complacent by years of peacetime prosperity, outsourcing, and digital convenience:

We need to build a permanent, long-term, realistic strategy for the future of America — economic growth, fiscal policy, industrial policy, foreign policy. We need to educate our citizens. We need to take control of our economic destiny.

This isn’t a partisan appeal — it’s a sobering wake-up call. Because our economy and military readiness are not separate issues. They are deeply intertwined.

Dimon isn’t alone in raising concerns. Former Google CEO Eric Schmidt has warned that China has already overtaken the U.S. in key defense technologies — hypersonic missiles, quantum computing, and artificial intelligence to mention a few. Retired military leaders continue to highlight our shrinking shipyards and dwindling defense manufacturing base.

Even the dollar, once assumed untouchable, is under pressure as BRICS nations work to undermine its global dominance. Dimon, notably, has said this effort could succeed if the U.S. continues down its current path.

So what does this all mean?

RELATED: Is Fort Knox still secure?

It means we are living in a moment of stunning fragility — culturally, economically, and militarily. It means we can no longer afford to confuse digital distractions with real resilience.

It means the future belongs to nations that understand something we’ve forgotten: Strength isn’t built on slogans or algorithms. It’s built on steel, energy, sovereignty, and trust.

And at the core of that trust is you, the citizen. Not the influencer. Not the bureaucrat. Not the lobbyist. At the core is the ordinary man or woman who understands that freedom, safety, and prosperity require more than passive consumption. They require courage, clarity, and conviction.

We need to stop assuming someone else will fix it. The next crisis — whether military, economic, or cyber — will not politely pause for our political dysfunction to sort itself out. It will demand leadership, unity, and grit.

And that begins with looking reality in the eye. We need to stop talking about things that don’t matter and cut to the chase: The U.S. is in a dangerously fragile position, and it’s time to rebuild and refortify — from the inside out.

Want more from Glenn Beck? Get Glenn's FREE email newsletter with his latest insights, top stories, show prep, and more delivered to your inbox.

Coinbase received an extortionary email asking for $20 million in ransom from hackers who said they had obtained private user data.

The cryptocurrency exchange platform said a May 11 message demanded the money in return for not publicly disclosing information that was obtained through Coinbase employees.

'No passwords, private keys, or funds were exposed, and Coinbase Prime accounts are untouched.'

In a press release, Coinbase said "cyber criminals bribed and recruited" "rogue overseas support agents" to steal customer data in order to facilitate social engineering attacks.

Coinbase described the intrusion as only affecting a small subset of customers (less than 1%). However, this could still account for more than 1 million app users, given 2024 estimates that the company had ballooned to 105 million users, according to Business of Apps.

"No passwords, private keys, or funds were exposed, and Coinbase Prime accounts are untouched," Coinbase noted. "We will reimburse customers who were tricked into sending funds to the attacker."

While the company did its best to reassure its customers, a plethora of private information was swept up that users will not be happy about.

RELATED: Senate rejects cryptocurrency bill pushed by Treasury Sec. Bessent

According to Coinbase, hackers were provided with user names, addresses, phone numbers, and emails. The last four digits of Social Security numbers, masked bank account numbers, images of government ID, and more were allegedly stolen as well.

Dean Gefen, CEO of cybersecurity firm NukuDo, told Blaze News that this kind of data breach has long-term effects that most will come to realize.

'That kind of exposure isn't just a privacy issue; it opens the door to phishing, identity theft, and long-term financial vulnerability. Most users won't feel it today, but if that data gets sold or abused, the impact will remain for years."

Gefen explained that the reason crypto account holders are so at risk is because they sit at the intersection of finance and emerging tech. These two sectors often move ahead at light speed and end up leaving security in the rearview mirror, hoping to catch up.

"Any company storing sensitive financial data needs to take this as sign to be on notice. Without the right people, training, and systems in place, this kind of breach is inevitable," Gefen said.

— (@)

When asked if this was just the cost of doing business at this scale, Gefen replied, "[Only] if we accept failure as normal."

"We wouldn’t tolerate this kind of breach in a nuclear facility or defense system, so why would we accept it in our financial infrastructure?"

The cybersecurity expert added that bad actors from China, North Korea, and Russia are among the biggest threats who look at crypto platforms as attractive, decentralized targets.

Coinbase said that is working with "industry partners" and law enforcement to connect the dots, but instead of paying the ransom, it planned to establish a $20 million reward fund for information leading to the arrest and conviction of the attackers.

The crooked insiders were allegedly "fired on the spot" and referred to "U.S. and international law enforcement."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Democrats do not want the specious nature of their charge of racism to be revealed, let alone adjudicated.

Democrats do not want the specious nature of their charge of racism to be revealed, let alone adjudicated.

The American people deserve financial institutions that serve all law-abiding citizens, not just those who align with the ruling class’s preferred ideology.

The American people deserve financial institutions that serve all law-abiding citizens, not just those who align with the ruling class’s preferred ideology.

Once a low-cost haven for service members, veterans, and their families, USAA’s troubles suggest a company prioritizing leftist ideology over its mission.

Once a low-cost haven for service members, veterans, and their families, USAA’s troubles suggest a company prioritizing leftist ideology over its mission.