America tried to save the planet and forgot to save itself

Let’s face it: $20 trillion is a lot of money.

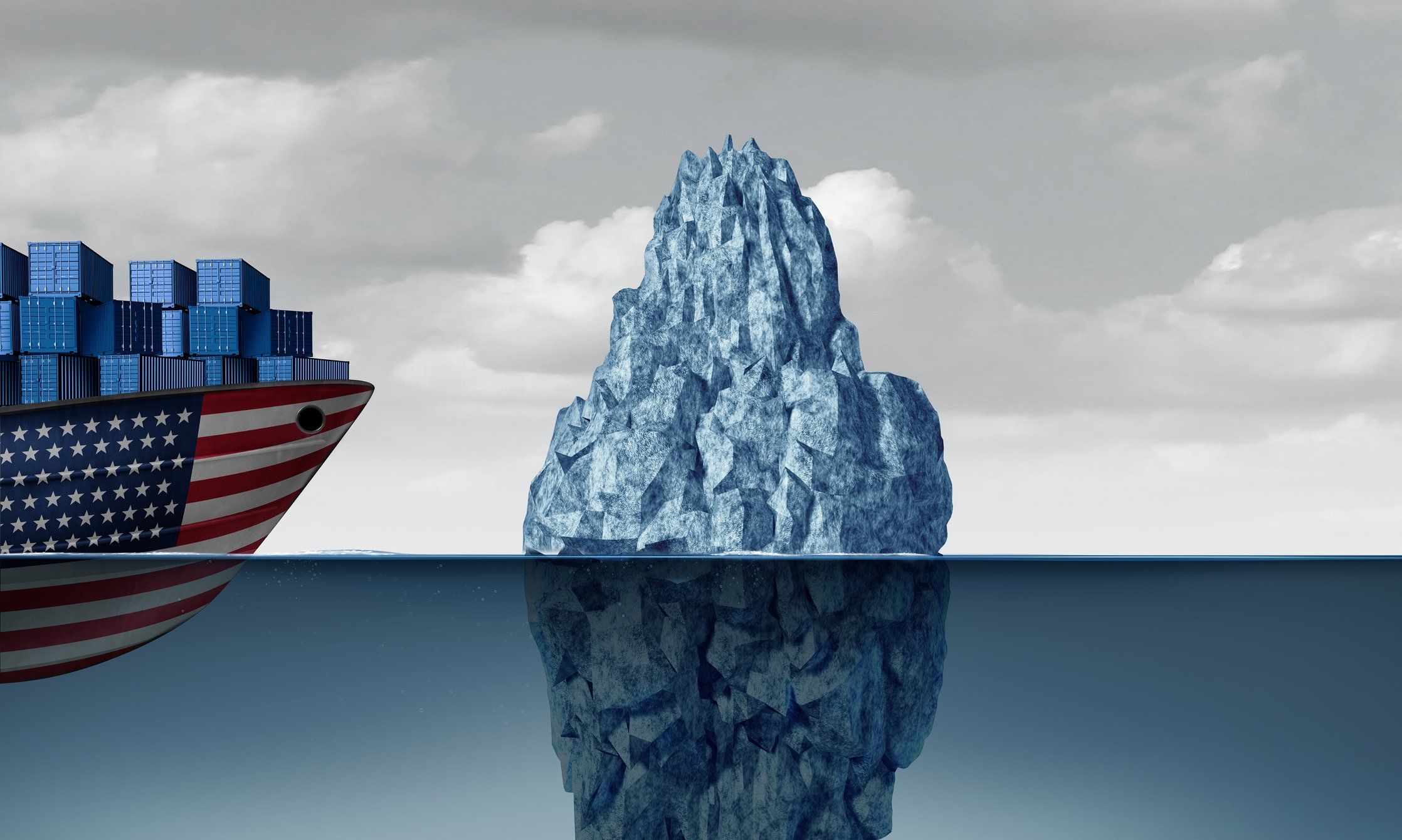

One would expect a big bang to follow the spending of 20,000 billion dollars. It’s a lot of money! In fact, it’s pretty much the total present value of America’s GDP.

The American economy sent trillions to our south and east — putting America second, hollowing out the American middle class, and neutralizing the American dream.

This is the total amount spent globally — largely by Europe and the United States — in a coordinated effort by the developed world to decarbonize the global economy. China, in contrast, sold windmills and solar panels worldwide while opening a new coal-fired power plant every month.

What was the net effect of this “Green" Marshall Plan? Hydrocarbon consumption continued to increase anyway. All that was achieved was a tiny reduction, just 2%, in the share of overall energy supplied by hydrocarbons. Put simply, as the energy pie got bigger and all forms of energy supply increased, hydrocarbons ended up with a slightly smaller share of a larger pie.

We also saw the deindustrialization of the European and American economies — not just with higher prices at the gas pump and on electric bills, but a stealth green tax that was passed on to consumers on everything. This is the culprit of our American and global affordability crisis. So much treasure and pain for a 2% reduction in the share of hydrocarbons.

Ironically, a byproduct of this Green Hunger Games was political populism.

What a waste. The worst bang for the public and private buck ever. Yet the Chicken Little believers of the Church of Settled Science and the grifters who profited from it will still sing in unison that it failed because they did not go far enough. If only the global community spent and regulated more!

In contrast, the Marshall Plan (1948-1951) rebuilt a decimated Europe into an industrial, interconnected, and peaceful powerhouse. It was a great success by any measure. At the time, its price tag was huge: $13.3 billion in nominal 1948-1951 dollars, equivalent to approximately $150 billion in today’s dollars.

Since a trillion is such a large number, let’s divide $20 trillion by an inflation-adjusted Marshall Plan of $150 billion, and we have 133 Marshall opportunities. Money was not the problem. To give a sense of the comparative bang for buck, by the Marshall program’s end, the aggregated gross national product of the participating nations rose by more than 32% and industrial output increased by a remarkable 40%.

President Trump has been on the global funding rounds and has secured more than $18 trillion in foreign investment. That’s roughly the equivalent of 120 Marshall Plans — just 13 shy of $20 trillion — to be invested here and nowhere else.

Unlike NAFTA, through which the rich got richer under the banner of free markets in exchange for cheaper consumer goods, Trump’s policy is a recipe for prosperity for all Americans.

RELATED: Trump administration saves billions in simple move globalists and climate activists alike will hate

Making these investments a reality in America will require a growing army of blue- and white-collar workers. With the wealth that it creates, our debt could be paid down and, finally, retired. Social Security and Medicare would be placed on a solid footing for time immemorial. All our public obligations to one another would be met by ever-growing prosperity, not by borrowed money and suffocating debt service.

Nothing approaching this level of intentional investment in a single country has ever been done. Yes, a similar tranche of greenbacks was burned with no discernible environmental benefit and great economic hardship for all. And yes, the American economy, under the guise of comparative advantage, sent trillions to our south and east — putting America second, hollowing out the American middle class, and neutralizing the American dream.

Trump’s plan is the opposite of both failed experiments. Like the original Marshall Plan, Trump’s is a recipe for the reindustrialization of the American economy and military, and it is not going to be fueled by windmills and solar farms but with hydrocarbons and uranium. That’s the Trump plan. It has merit.

Yet if we look at the polls, Trump is under water, and his base is showing signs of stress fractures. You bring peace to the Middle East, stop six other wars, and bring in some $20 trillion in America First investments within your first year, and you come home to find yourself under water and called a “lame duck.” Democracies are known to be fickle and hard to please, but this is still rich — and it will result in poverty if it continues.

Without the use of Trump’s tariffs and dealmaking, there would not be $20 trillion looking to onshore in the United States. You can blame Trump for higher costs on bananas and coffee, but it is the cost of electricity and health care — not the cost of coffee and bananas — that is roiling kitchen-table economics.

Vice President JD Vance recently made the right call for popular and populist patience. Those who are impatient should look at the offsets already passed, such as no taxes on Social Security, tips, and overtime. That helps pay for bananas and coffee and then some.

The sovereign wealth funds that are presently lining up on our shores are coming here based on promises made by a can-do president speaking for a can-do nation. While Trump is a can-do guy, are “We the People” still a can-do people? Or do we at least want to return to becoming a can-do people again?

The “can’t-do” forces are legion, and they are the ones now championing the affordability crisis they caused. When America was a can-do nation, we built the Empire State Building in a year. Today, it would take years to get a permit.

RELATED: From Monroe to ‘Donroe’: America enforces its back yard again

Those willing to invest such money will require some certitude that the power they will need will be there to “build, baby, build.” If not, the money and the opportunity will pass before they have the possibility to take needed root.

And what about us, the American family, worker, and business continuing to struggle under the legacy of throttling energy privation? In short, we all have a common good — a shared interest — in righting the wrongs that control our grid and our nation’s future.

The good news is that a bill was introduced in the House during the government shutdown. It’s called the “Affordable, Reliable, Clean Energy Security Act.” Unlike Obamacare, which clocked in at 903 pages, this bill is a lean 763 words. If it becomes law — and it should — it would change everything for the better, unlike Obamacare, which is a recipe for unaffordability.

Trump’s One Big Beautiful Bill Act was missing this one thing. His short- and long-term America First ambitions would be significantly strengthened by making this energy bill law before the midterms. Executive orders don’t provide the energy security these investors require or the American people deserve.

$20 trillion is a lot of money. Coming to our shores is a new lease on the American experiment as we enter our 250th birthday, hopelessly divided and broke. Let us come together to solve not just the affordability crisis but also set the conditions for greatness for the next 250 years.

Editor’s note: This article was originally published by RealClearPolitics and made available via RealClearWire.

Photo by Andrew Harnik/Getty Images

Photo by Andrew Harnik/Getty Images MediaProduction via iStock/Getty Images

MediaProduction via iStock/Getty Images

Ekaterina Chizhevskaya via iStock/Getty Images

Ekaterina Chizhevskaya via iStock/Getty Images