![]()

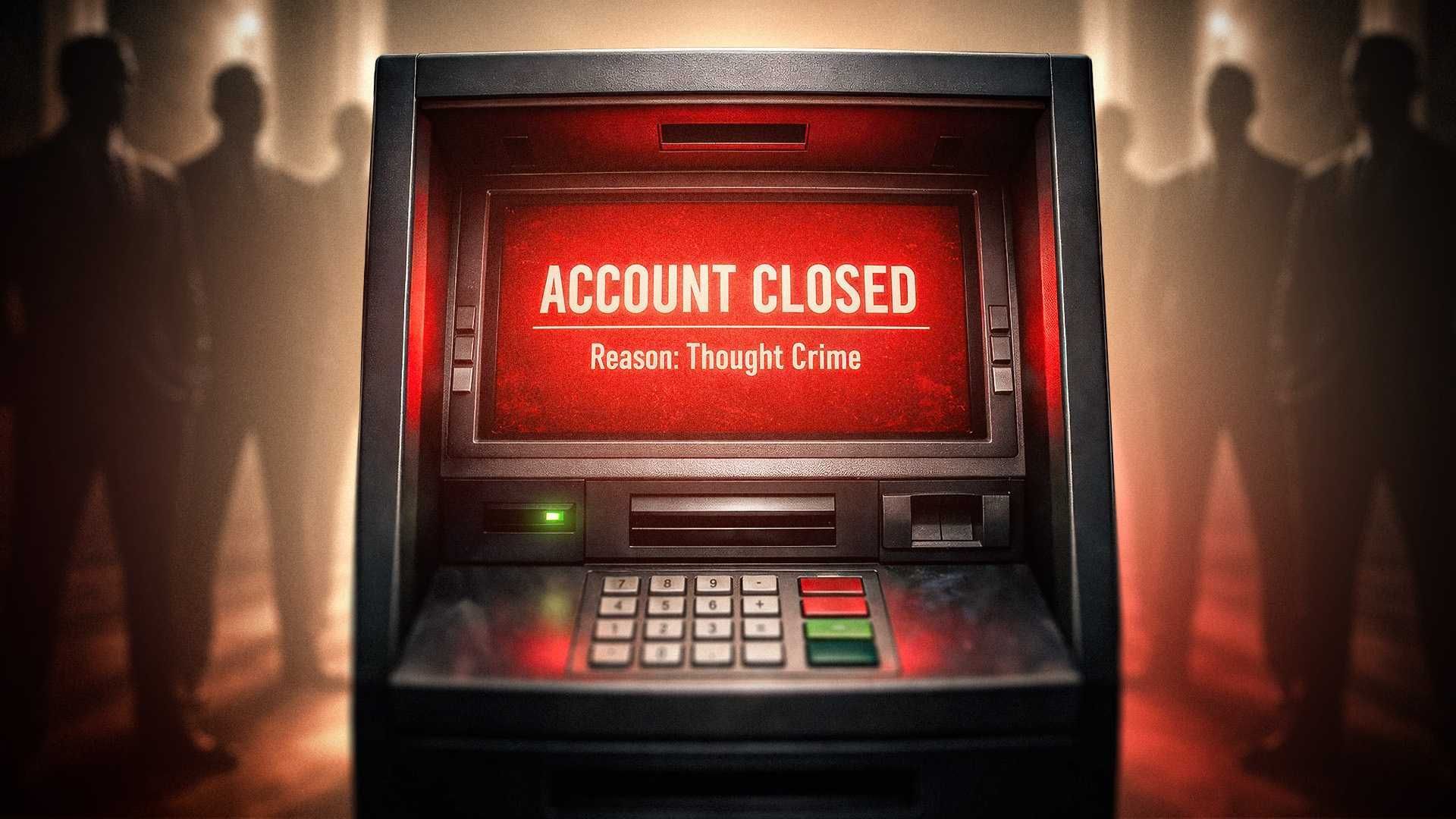

Most Americans assume that if their deposits are insured, their banking relationship is stable.

For decades, that assumption has been reasonable. Large national banks offer scale, convenience, and integration across checking, credit cards, mortgages, investments, and digital tools. For many households and businesses, they remain the default choice — for many good reasons.

Regional and community banks typically face fewer reputational signaling incentives and fewer reasons to police customers’ lawful beliefs.

But in recent years, some lawful customers have found accounts restricted or closed not for fraud or criminal conduct, but because the financial institution decided internally that the customer is a risk to the institution's reputation or political standing. In other words: They have been canceled.

These cases are often hard to prove — and that difficulty is itself the problem. First lady Melania Trump revealed in her memoir that a bank decided to "terminate" her account. The reasoning was frustrating to pin down, since decisions on account restrictions are shielded from public verification by opaque risk explanations and confidentiality rules.

Other cases were clearer. In 2023, internal documents revealed that U.K. private bank Coutts closed the account of British politician Nigel Farage after deciding his political views posed “reputational risk” — a disclosure that ultimately led to the resignation of National Westminster Bank's chief executive.

“If they can do it to me, they can do it to you, too,” Farage proclaimed after the dispute.

The risk

Your money may be insured, but access to it is governed by institutional judgment. For some consumers, understanding where that judgment lies is now part of responsible financial planning.

That’s where this guide comes in. It’s not a broadside against megabanks. It is a road map for readers who want to understand the trade-offs that come with scale — particularly when account access is governed by broad, centralized risk frameworks rather than personal relationships or clearly defined misconduct.

Regulators have since moved to clarify standards governing account closures and risk assessments. But for consumers who watched large institutions end financial relationships under ambiguous or shifting rules, the question remains straightforward: Why assume that risk if alternatives exist?

There are no guarantees. But there are differences — rooted in structure, incentives, and how close a branch is to customers — that can meaningfully affect how ideological risk is handled.

Ideological risk is not evenly distributed. It tends to correlate with scale, distance, and discretion, rather than with partisan labels.

This guide organizes banks into categories based on structure and incentives, not ideology.

How this list was compiled

All banks listed below meet the following baseline criteria:

- FDIC-insured (or equivalent federal backing).

- No public record of ideologically motivated account closures.

- Standard modern banking services, including online and mobile access.

- Responses to Align's inquiries, where available.

- Institutional cultures or policies emphasizing lawful, viewpoint-neutral customer treatment.

Banks to consider

1. Regional and community banks

They are often safer. Regional and community banks typically operate on relationship-based models, with decision-making closer to customers and local markets. They face less national activist pressure, fewer reputational signaling incentives, and fewer reasons to police customers’ lawful beliefs.

Here’s what to look for:

- FDIC insurance.

- Rigorous underwriting standards.

- Focus on local business, agriculture, manufacturing, or regional commerce.

- Long operating histories.

- Knowing exactly who to talk to next if your problem isn't fixed.

Warning: Not all community banks are equal. Some rely heavily on third-party compliance vendors or adopt national risk frameworks wholesale. Size alone is not a guarantee.

Here are some strong options.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.8 (32.2K reviews); Apple 4.8 (47K reviews)

Region/States: 730+ branches in 17 states

ATM: MoneyPass network

Woodforest National Bank is a privately owned, community-focused financial institution headquartered in The Woodlands, Texas, that has provided banking services since 1980, operating hundreds of branches across multiple states and offering products for both personal and business customers. It offers a full range of financial services including checking and savings accounts, loans, debit cards, online and mobile banking, and other products designed for everyday banking needs. The bank emphasizes customer relationships, convenient access — including retail locations and digital tools — and a commitment to serving the communities where its customers live and work.

FDIC-insured: Yes

Credit card: Yes (via Premier Bankcard)

App: Yes — Google 4.5 (1.48K reviews); Apple 4.4 (1.4K reviews)

Region/States: 13 branch locations in South Dakota

ATM: Fee-free access to 37,000+ MoneyPass ATMs nationwide

First Premier Bank is an independently owned, FDIC-insured community bank headquartered in Sioux Falls, South Dakota. It offers a full range of financial products and services, including personal, business, and agricultural checking and savings accounts, loans and mortgages, wealth management, and digital banking. The bank also operates Premier Bankcard, a nationally recognized issuer of Mastercard credit products. First Premier emphasizes strong capitalization, customer support, community investment, and accessible online and mobile banking tools for managing finances nationwide.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.7 (987 reviews); Apple 4.8 (9.7K reviews)

Region/States: 24 locations in Dallas-Fort Worth

ATM: ATMs at nearly all branches

American National Bank of Texas is a long-established, independently owned, FDIC-insured community bank headquartered in Terrell, Texas, with more than 30 branches serving North Texas. It offers a full suite of financial products and services including personal and business checking and savings, loans and mortgages, digital banking, and wealth management. The bank emphasizes local relationship-driven service, community involvement, and comprehensive financial solutions tailored to individuals and businesses alike.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.9 (15 reviews); Apple 4.6 (192 reviews)

Region/States: 18 locations in Iowa, South Dakota, Nebraska

Liberty National Bank (Midwest) is an independently owned, FDIC-insured community bank headquartered in Sioux City, Iowa, founded in 2003. With approximately $600 million in assets, it serves customers across Iowa, South Dakota, and Nebraska, including Sioux City, Sioux Falls, and surrounding communities. The bank emphasizes local decision-making, relationship-based service, and support for families, businesses, and agricultural clients in the markets it serves.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.5; Apple 4.9

Region/States: ~10 locations in Oklahoma and North Texas

ATM: 20 local ATMs

Liberty National Bank (Texas/Oklahoma) is an independently chartered, FDIC-insured community bank headquartered in Lawton, Oklahoma. Originally established in 1902 as the Bank of Elgin, it adopted the Liberty National name in 2002 and has since expanded across Oklahoma and into North Texas, with assets exceeding $1 billion. The bank remains under Green family ownership and emphasizes long-standing ties to local communities, regional growth, and personalized banking relationships.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.6 (322 reviews); Apple 4.8 (1.1K reviews)

Region/States: 33 locations in California

ATM: Pulse & Cirrus (400,000 ATMs)

Farmers & Merchants Bank of Central California offers personal and business banking services, including a variety of checking and savings accounts, loans, and agricultural financing tailored to individuals and companies across numerous California communities. The website emphasizes secure 24/7 online and mobile banking so that customers can manage accounts, transfer funds, pay bills, and access eStatements from anywhere. It also highlights local branch access, community roots dating back over a century, and a commitment to serving customers’ financial needs.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 2.8 (82 reviews); Apple 4.6 (790 reviews)

Region/States: 18 locations in Virginia, West Virginia, Tennessee, North Carolina

ATM: Allpoint (55,000 locations)

New Peoples Bank is a community-focused financial institution with multiple branches serving individuals and small to medium-size businesses across Southwestern Virginia, Southern West Virginia, Northeastern Tennessee, and Western North Carolina, offering a full suite of personal and business banking products including checking, savings, loans, and online services. Through its website, customers can open accounts, apply for mortgage or personal loans, manage finances with online and mobile banking tools, and access additional services like identity protection and ATM networks. The bank emphasizes local decision-making, Golden Rule customer service, and technology that supports secure, convenient banking experiences.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 3.8 (51 reviews); Apple 4.8 (431 reviews)

Region/States: 7 locations in Kentucky

ATM: MoneyPass

First United Bank and Trust Company is a community-oriented, FDIC-insured bank offering a full range of personal and business financial services, including checking and savings accounts, loans, digital banking, and trust solutions accessible online or at local branches. The bank emphasizes convenient 24/7 access to accounts, tools for managing finances, and solutions like credit cards and business services tailored to local needs. Its website highlights personal service, community engagement, and products designed to support customers’ financial goals with trusted relationships and modern banking technology.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.4 (132 reviews); Apple 4.8 (399 reviews)

Region/States: 6 locations in Iowa and Nebraska

ATM: MoneyPass

Arbor Bank is a community FDIC-insured bank offering a wide range of personal and business financial products, including checking and savings accounts, online/mobile banking, lending solutions, and mortgage services. It also provides business banking tools like treasury management, SBA loans, and positive pay fraud protection, along with card solutions and insurance options. The website emphasizes secure digital access, personalized service, and support for customers’ financial growth.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 3.6 (82 reviews); Apple: 4.6 (1.5K reviews)

Region/States: Over 750 First Command Bank advisers in over 175 offices in 45 states and Guam

ATM: MoneyPass ATM network and NYCE network; reimburses non-FCB ATM surcharges up to $10 per statement cycle

First Command’s banking section highlights personal banking products tailored for military personnel, veterans, and their families, including competitive checking and savings accounts, CDs, car loans, and debt consolidation options. These services come with convenient online and mobile access so that customers can manage funds, pay bills, and transfer money securely from anywhere, backed by the FDIC-insured protection First Command Bank offers. The emphasis throughout is on helping service members and their families manage everyday finances and build solid financial habits.

FDIC-insured: Yes

Credit card: No (mobile app offers free credit report updates weekly)

App: Yes — Google: 4.7 (1.24K reviews); Apple: 4.8 (3.1K reviews)

Region/States: 19 locations in Florida (The Villages and surrounding counties)

ATM: On-site ATMs at most branch locations; part of the Publix Presto! ATM Network (1,300+ surcharge-free ATMs across the Southeast); additional access through regional shared ATM arrangements (fees may vary depending on network)

Citizens First Bank is an FDIC-insured community bank serving The Villages and surrounding counties in Florida. It offers personal and business checking and savings products, robust online and mobile tools including bill pay and eStatements, and an ATM network focused on surcharge-free access. The bank merged with Seacoast Bank in October 2025 following the acquisition of its parent company, with conversion of accounts tentatively scheduled for July 2026.

FDIC-insured: Yes

Credit card: No

App: No dedicated mobile app; online account management via EmigrantOnline®

Region/States: 2 locations in New York; 1 location in Miami, Florida

ATM: On-site ATMs at branch locations; The bank refers to participation in ATM networks, though specific network details and surcharge policies are not prominently disclosed on its website. Prospective customers should confirm ATM access and fee policies directly with the bank.

Emigrant Bank is a privately owned U.S. financial institution offering high-yield savings, checking accounts, CDs, and mortgage lending. It emphasizes competitive deposit products and online/telephone banking access rather than a large retail branch footprint. Emigrant also provides mortgage lending through its direct lending division and support for account holders with tools to handle funds and financial needs securely.

2. Credit unions

Credit unions are member-owned, less PR-sensitive, and historically focused on service rather than signaling. Because there are thousands of local credit unions with varying eligibility rules, this guide does not list specific institutions.

How to find a good one:

- Confirm NCUA insurance.

- Look for long operating histories.

- Favor credit unions with business or agricultural lending.

- Ask directly about account-closure policies and escalation.

3. Explicitly viewpoint-neutral banks

This is the smallest and most visible category — and the one that requires the most due diligence before joining.

The claim here is not that these banks are “conservative,” but that they have made explicit commitments to viewpoint neutrality and have no public record of ideological account closures.

What qualifies:

- Public neutrality policies.

- Leadership statements emphasizing lawful activity over belief.

- Clear articulation of when accounts would be restricted.

- No documented ideological de-banking cases.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.6 (940 reviews); Apple 4.8 (1.5K reviews)

Region/States: Nationwide digital access; one physical branch

ATM: MoneyPass (40,000+ ATMs)

Old Glory Bank is a full-service, FDIC-insured American bank headquartered in Elmore City, Oklahoma, offering personal and business checking and savings accounts, loans, certificates of deposit, and modern digital tools like mobile and online banking with nationwide access. It positions itself as a nationwide online bank built around traditional American values and strong commitments to privacy, security, and customer autonomy. Customers can bank digitally from all 50 states while also accessing features such as ATM networks, cash deposit options, and advanced debit card controls.

Co-founded by John Rich, Dr. Ben Carson, Larry Elder, and former Oklahoma Gov. Mary Fallin (R), Old Glory is guided by what it calls the Banking Bill of Rights. A statement to Align from the founders makes the bank’s stand against de-banking central to its mission: “Not only does Old Glory Bank have a policy on de-banking, it is the very reason we exist! We were founded in direct response to the growing and troubling practice of de-banking Americans for their lawful, constitutionally protected beliefs. We saw the alarming trend in January 2021 and got to work years before it became newsworthy. We stand firm on the belief that this practice is morally, legally, and fundamentally incompatible with the freedom upon which our nation was built.”

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.8 (21 reviews); Apple 4.9 (523 reviews)

Region/States: 7 locations in Oklahoma, Texas, Missouri

ATM: 10 free out-of-network transactions monthly

Regent Bank is a regional, FDIC-insured, full-service bank headquartered in Tulsa, Oklahoma, with multiple branches in Oklahoma, Texas, and Missouri, offering personal and business banking products including checking, savings, loans, digital banking, and treasury services. It emphasizes personalized, concierge-style service tailored to entrepreneurs, small and mid-market businesses, and specialized niches like health care, agriculture, and nonprofits. The bank combines traditional community banking values with modern tools and solutions, supporting clients’ financial needs through dedicated local relationships and digital access.

A Regent Bank spokesperson told Align that the institution identifies as a “Christian, faith-based organization in terms of [its] mission and values” and that its “approach is grounded in relationship-driven banking and serving clients based on lawful activity — not political or religious beliefs.” Regent’s spokesperson added that de-banking is a frequently discussed issue at the executive level of the organization.

4. Large regional and super-regional banks

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.5 (128K reviews); Apple: 4.9 (521K reviews)

Region/States: 1,445 locations across 15 states spanning the South, Midwest, and Texas

ATM: No-fee access at Regions ATMs

Regions Bank is a large, FDIC-insured, full-service financial institution and subsidiary of Regions Financial Corporation, offering a broad range of personal banking products including checking and savings accounts, loans and mortgages, digital banking, and wealth management solutions. It serves millions of customers through an extensive branch and ATM network across the South, Midwest, and Texas, while also providing online and mobile tools for everyday account management The bank combines traditional community-oriented service with modern digital convenience to support a wide spectrum of consumer financial needs.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.6 (6.8K reviews); Apple: 4.7 (29K reviews)

Region/States: ~20 branches in Utah and other Western markets

ATM: No-fee ATM network serving Western U.S.

Zions Bank is a full-service, FDIC-insured regional bank operating as part of Zions Bancorporation, offering personal banking products such as checking and savings accounts, loans and mortgages, credit cards, and robust digital banking tools including online and mobile access. It serves individuals and small businesses through an extensive network of full-service branches across multiple Western states and emphasizes community-focused service with modern financial solutions. Founded in the 19th century and rooted in local market relationships, Zions Bank combines traditional banking values with convenient digital access for everyday financial management.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 4.7 (10.6K reviews); Apple: 4.8 (50K reviews)

Region/States: 40+ locations in Alabama and Georgia

ATM: Unlimited fee-free Pinnacle Financial Partners ATMs

Synovus is a large, FDIC-insured financial services company and bank holding company headquartered in Columbus, Georgia, offering a full range of commercial and personal banking products including checking and savings, loans, mortgages, credit cards, and digital banking. It also provides specialized services such as wealth management, trust and investment solutions, treasury management, and mortgage and capital markets services through its subsidiaries. Synovus operates an extensive branch and ATM network across the Southeast and emphasizes personalized client relationships alongside modern digital tools.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google: 3.6 (12.5K reviews); Apple: 4.9 (252K reviews)

Region/States: 310 locations in Arkansas, Kansas, Missouri, and Oklahoma

ATM: Offers ATMs with live teller drive-thru services

Arvest Bank is a regional full-service bank offering personal and business financial products including checking and savings accounts, loans and mortgages, credit cards, wealth and treasury management, and secure online and mobile banking tools. Through its extensive network of branches across Arkansas, Oklahoma, Missouri, and Kansas, the bank emphasizes local community commitment while providing modern digital conveniences like 24/7 account access and mobile deposits. Its mission centers on partnering with customers to deliver tailored financial solutions that support everyday banking needs and long-term financial goals.

FDIC-insured: Yes

Credit card: Yes

App: Yes — Google 4.5 (1.3K reviews); Apple 4.9 (8.7K reviews)

Region/States: 55 branches across Texas, including Austin, Corpus Christi, Dallas, Fort Worth, Houston, Lubbock, San Antonio, and the Rio Grande Valley

ATM: Branch and regional network ATM access (confirm surcharge policies directly with bank)

Founded in 1988 in Lubbock, Texas, PlainsCapital Bank has grown into one of the largest independent banks in the state, with approximately $12.4 billion in assets and more than 1,000 employees. A subsidiary of Hilltop Holdings Inc., it operates a statewide branch network and offers commercial banking, treasury management, private banking, wealth management, and consumer banking services. While emphasizing relationship-based banking, PlainsCapital functions at the scale of a large regional institution with centralized infrastructure and enterprise-level risk management.

What to approach with caution

Not every “alternative” bank actually reduces ideological risk.

- Fintech apps without their own bank charter: Many rely on sponsor banks and payment processors, meaning account access can be restricted upstream with little notice.

- Institutions with expansive “reputational risk” clauses: Banks that reserve broad discretion to sever relationships for social or political reasons introduce uncertainty.

- Ideological startups without federal backing: Branding is not a substitute for FDIC insurance, balance-sheet transparency, or regulatory oversight.

Questions to ask your bank

If ideological or reputational risk is a concern, you don’t need to announce your politics or interrogate your bank. You’re simply trying to understand process, discretion, and escalation — the same way you would with fees, fraud protection, or data security.

These are reasonable, neutral questions.

1. Under what circumstances can my account be restricted or closed?

Listen for clear references to fraud, illegality, or operational risk. Be cautious if you hear broad or undefined references to “reputational,” “social,” or “values-based” concerns.

2. Will I receive notice before an account is restricted or closed?

Ask:

- How much notice is typical?

- Are there circumstances under which notice is not provided?

Advance notice reduces risk regardless of ideology.

3. Is there an appeal or escalation process if a decision is made?

Important follow-ups:

- Can decisions be reviewed by a human committee?

- Is there a relationship manager or ombudsman involved?

The ability to appeal matters as much as the rule itself.

4. Who ultimately makes account-closure decisions?

You’re listening for local or relationship-based decision-making versus centralized compliance teams or third-party vendors. Distance often correlates with opacity.

5. Do you rely on third-party compliance or risk vendors?

This matters because:

- Upstream vendors can impose restrictions that the bank itself did not initiate.

- Vendor changes can alter outcomes without warning.

6. How do you define “reputational risk”?

A strong answer ties reputational risk to concrete financial, legal, or operational exposure.

A weak answer uses vague or moralized language without boundaries.

7. Are account decisions based on lawful activity, regardless of belief or affiliation?

Banks that can say this plainly usually mean it.

8. Is my account subject to special monitoring or enhanced review?

This is especially relevant for nonprofits, small businesses, and public-facing individuals.

How to use this checklist

You don’t need perfect answers. You’re looking for a bank that can explain its rules clearly — and show how decisions are reviewed.

Photo by Michael Tullberg/Getty Images

Photo by Michael Tullberg/Getty Images

Just_Super via iStock/Getty Images

Just_Super via iStock/Getty Images AndreyPopov via iStock/Getty Images

AndreyPopov via iStock/Getty Images

natasaadzic/iStock/Getty Images Plus

natasaadzic/iStock/Getty Images Plus Mininyx Doodle/iStock/Getty Images Plus

Mininyx Doodle/iStock/Getty Images Plus It has an object of worship, which is female autonomy, its own commandments, theological virtues, a sacrament, and even its own form of evangelization.

It has an object of worship, which is female autonomy, its own commandments, theological virtues, a sacrament, and even its own form of evangelization.

Photo by Andrew Lichtenstein/Corbis via Getty Images

Photo by Andrew Lichtenstein/Corbis via Getty Images

Stefani Reynolds/Bloomberg via Getty Images

Stefani Reynolds/Bloomberg via Getty Images In 'The Transhumanist Temptation,' Grayson Quay unmasks a pernicious ideology that even those most opposed to it are having trouble resisting.

In 'The Transhumanist Temptation,' Grayson Quay unmasks a pernicious ideology that even those most opposed to it are having trouble resisting.

Blaze Media Illustration

Blaze Media Illustration