![]()

Kevin Warsh, the primary intermediary between the Federal Reserve and Wall Street during the 2008 financial crisis, was confirmed on Tuesday to a 14-year term as Federal Reserve governor and confirmed on Wednesday as Jerome Powell's successor as chairman of the U.S. central bank.

Powell, who was first nominated to the Federal Board of Governors by former President Barack Obama and whose term as chair ends on Friday, wished Warsh well. However, he also provided his replacement with something more valuable than a nice sentiment: examples of what not to do, or at least, what to avoid doing.

Powell has, after all, dropped the ball on numerous occasions — sometimes with catastrophic consequences for the country. Here are just four examples.

1. Don't worry, it's 'transitory.'

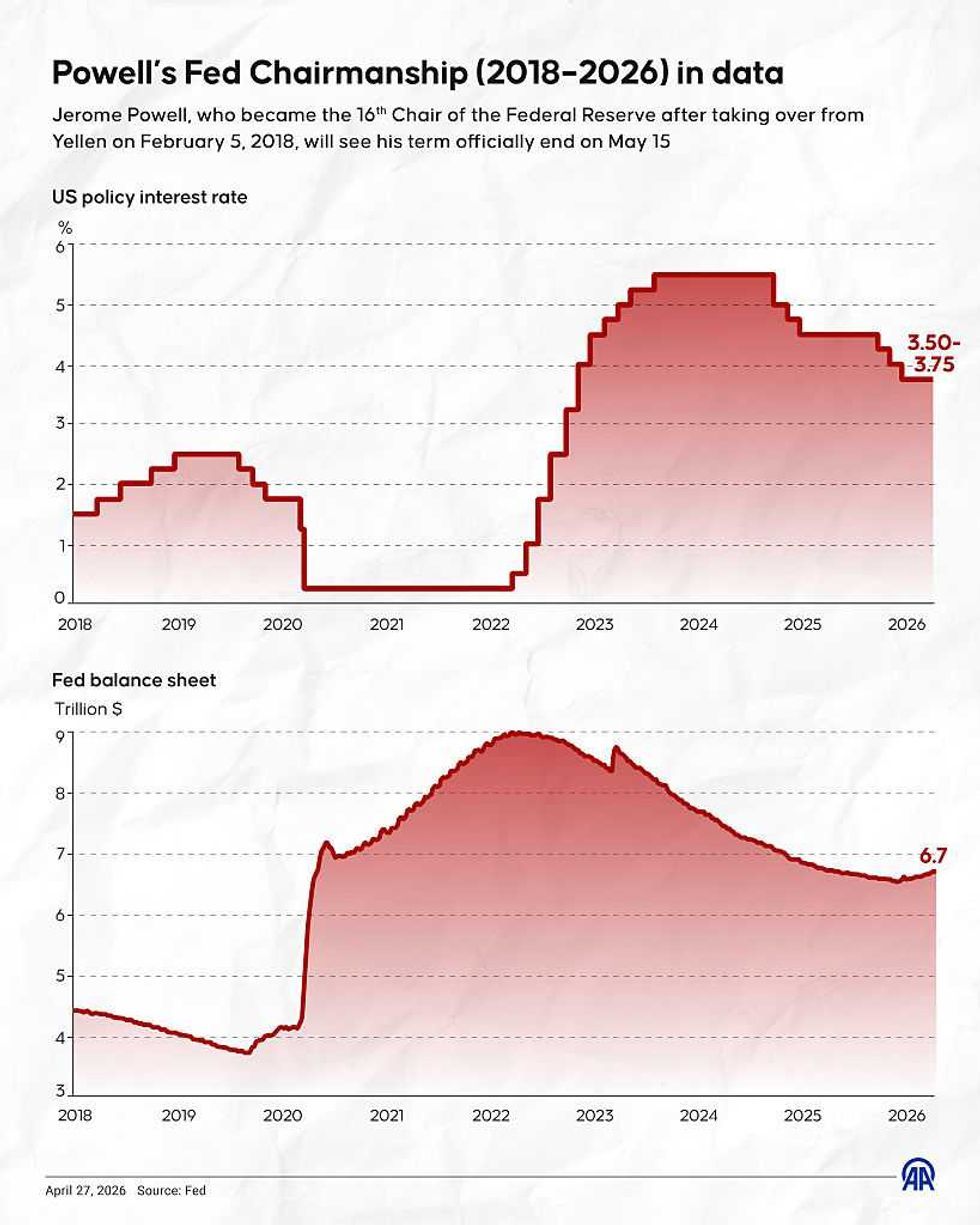

Powell stated on March 4, 2021, in the second year of the pandemic, that inflation might increase but that it would likely be "transitory" and not enough for the central bank to raise record-low interest rates — a decision some suspect was geared toward pleasing then-President Joe Biden and thereby securing Powell's reappointment.

'Most of the expected GDP slowdown — from over 3% to 1.5% — was due to Powell's blunder.'

MarketWatch's Greg Robb noted that Powell's wrong-headed "transitory" view of inflation — one that would define his eight years as Fed chair — precluded the Fed from raising interest rates until 2022 while the Fed was also buying up bonds "and swelling its balance sheet."

Thanks to Powell's mistake — which economist Mohamed El-Erian, former PIMCO chief executive, said was "probably the worst inflation call in the history of the Federal Reserve" — the Fed was consistently on the back foot.

RELATED: Your bank can shut you down overnight — here’s how to protect yourself

![]() Elif Acar/Anadolu/Getty Images

Elif Acar/Anadolu/Getty Images

Facing the highest inflation Americans had seen in 40 years — inflation that no longer appeared to be "transitory" — Powell ended up raising interest rates 11 times between March 2022 and July 2023, when its benchmark rate reached a range of 5.25% to 5.5%.

Powell told "60 Minutes" in a Feb. 1, 2024, interview:

In hindsight, it would've been better to have tightened policy earlier. I'm happy to say that. Really, it was this. We saw what we thought was that this inflation, which seemed to be mostly limited to the goods sector and to the supply chain story. We thought that the economy was so dynamic that it would fix itself fairly quickly. And we thought that inflation would go away fairly quickly without an intervention by us. That it would be transitory.

Powell leaves office with inflation well above the Fed's 2% target for five consecutive years.

2. Betting against Trump's tariffs, tax cuts

While reluctant initially to raise interest rates when Biden was in office, Powell previously demonstrated an eagerness to raise rates in 2018 when President Donald Trump was in office and the economy was booming.

"Every time we do something great, he raises the interest rates," Trump said at the time. Powell "almost looks like he's happy raising interest rates."

The repeated hikes, which Trump blamed for coinciding stock market turmoil, were supposedly prompted by concerns that the Republican president's tariffs and tax cuts, the latter of which were framed as a $1.5 trillion fiscal stimulus, might together contribute to inflation.

Powell stated that "fiscal policy is becoming more stimulative. In this environment, we anticipate that inflation ... will move up this year."

Economist Donald Luskin, chief investment officer for Trand Macrolytics LLC, recently noted that "there is no evidence that Mr. Trump’s tariffs in 2018 and 2019 led to any inflation at all."

Economist and Trump trade adviser Peter Navarro wrote last year, "Powell's audition for 'worst Fed chair' began shortly after his February 2018 appointment. Promising President Trump in the Oval Office a supportive posture to secure his nomination, Powell instead aggressively raised rates into the low-inflation, high-growth Trump economy. Powell wrongly believed Trump's tax cuts and tariffs would spark inflation — they didn't."

Powell's bet against Trump's tariffs and tax cuts proved consequential.

"As Powell's Fed hiked interest rates four times in 2018 — despite muted inflation and strong labor market gains — economic momentum slowed sharply," wrote Navarro. "According to the Fed's own September Tealbook, most of the expected GDP slowdown — from over 3% to 1.5% — was due to Powell's blunder."

"It would cost the American economy hundreds of thousands of jobs and hundreds of billions of dollars in lost economic output and tax revenues," added the trade adviser.

3. Fed renovation scandal

Powell reportedly greenlit luxury renovations to the Fed's Washington, D.C, headquarters that exceeded the original budget by roughly $700 million and is set to cost around $2.5 billion.

Controversy over the renovations — which include a rooftop terrace with gardens, VIP dining rooms, "premium" marble, and water features — came to a head in January, several months after U.S. Federal Housing Finance Agency Director William Pulte called for an investigation into Powell and his removal as Fed chair.

RELATED: Debit card company promises to pay your bill ... sometimes: 'Buy now, pay maybe'

![]() Sophie Park/Getty Images

Sophie Park/Getty Images

Powell said in a Jan. 11 statement that "the Department of Justice served the Federal Reserve with grand jury subpoenas, threatening a criminal indictment related to my testimony before the Senate Banking Committee last June. That testimony concerned in part a multiyear project to renovate historic Federal Reserve office buildings."

An activist Biden-appointed judge quashed the grand jury subpoenas in March.

"Jerome Powell today is now bathed in immunity, preventing my office from investigating the Federal Reserve," Jeanine Pirro, the U.S. attorney in Washington, said in response to U.S. District Court Judge James Boasberg's rulings. "This is wrong, and it is without legal authority."

Last month, the Trump administration dropped the criminal investigation into Powell over his luxury renovation project.

While apparently off the hook, the controversy nevertheless hangs over Powell as another example of costly mismanagement.

4. Bank failures

Powell and his underlings also failed to prevent the March 2023 collapses of Silicon Valley Bank and Signature Bank — the third- and fourth-largest bank failures in American history, respectively.

Powell acknowledged weeks after the bank failures that the Fed's efforts to intervene were too little, too late.

"It does kind of suggest there's a need for ... regulatory and supervisory changes, just because supervision and regulation need to keep up with what's happening," said Powell. "My only interest is that we identify what went wrong here ... make an assessment of what are the right policies to put in place so that doesn't happen again, and then implement those policies."

One of Powell's lieutenants, then-Vice Chair Michael Barr, admitted that the "Federal Reserve supervisors failed to take forceful enough action."

A damning April 28, 2023, report on the Fed's bungled supervision and regulation of Silicon Valley Bank — the conclusions of which Powell ultimately accepted — said that:

- "Federal Reserve supervisors did not fully appreciate the extent of the vulnerabilities as Silicon Valley Bank grew in size and complexity";

- "When supervisors did identify vulnerabilities, they did not take sufficient steps to ensure that Silicon Valley Bank fixed those problems quickly enough"; and

- "The Board's tailoring approach in response to the Economic Growth, Regulatory Relief, and Consumer Protection Act and a shift in the stance of supervisory policy impeded effective supervision by reducing standards, increasing complexity, and promoting a less assertive supervisory approach."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Democrats will spend the midterms trying to equate 'affordability' with more government spending programs. Conservatives should make the opposite case.

Democrats will spend the midterms trying to equate 'affordability' with more government spending programs. Conservatives should make the opposite case.

Michal Fludra/NurPhoto/Getty Images

Michal Fludra/NurPhoto/Getty Images

Elif Acar/Anadolu/Getty Images

Elif Acar/Anadolu/Getty Images Sophie Park/Getty Images

Sophie Park/Getty Images

Lawmakers focused on their reelection in a few months or years care little about whether the United States faces economic stagnation decades from now.

Lawmakers focused on their reelection in a few months or years care little about whether the United States faces economic stagnation decades from now. The president’s talk of a potential $500 million bailout for Spirit Airlines would deflate conservatives’ spirit at a critical juncture.

The president’s talk of a potential $500 million bailout for Spirit Airlines would deflate conservatives’ spirit at a critical juncture.