America’s ‘prosperity’ is built on broken families and debt

Ever since the COVID “Great Reset,” the American economy has functioned like a silent depression for two-thirds of households and most businesses. Washington pumped out biblical levels of spending and easy money, and a cycle of debt, high prices, and stagnation has crushed consumers.

Meanwhile, a handful of well-connected corporations — propped up by cheap credit, regulatory favors, and asset bubbles — keep the stock market afloat, creating the illusion of growth. The result is an economy that looks healthy on paper but feels like collapse on Main Street.

Enough. A nation cannot live on financial tricks and asset bubbles forever. Let the recession come.

The time has come to let it crash. No more bailouts. No more “too big to fail.” If we want a free-market recovery built on broad opportunity and wage-based wealth, we must let the bubbles burst.

The silent depression

Americans live under record-high prices for food, fuel, rent, and electricity. College graduates face the worst job market in decades. Payroll data shows just 1,494 new jobs were added in August — the weakest since the 2008 crash. Layoffs are up 38.5% this year.

For graduates, the outlook is even worse. Fortune reports that 58% of recent grads still can’t land a job or internship. Forty percent of the unemployed last year never even got an interview. One in five job seekers remained unemployed for 10 months or more.

Those already employed are struggling to make ends meet. Thirty-seven percent of workers have tapped retirement accounts for hardship withdrawals or loans. Personal spending, adjusted for inflation, fell 0.15% in the first half of 2025 — the sharpest decline since the financial crisis.

Families are drowning in debt. Household debt sits at $18.39 trillion, up $600 billion in one year. Student loans total $1.64 trillion, with more than 10% delinquent. Credit card debt has hit $1.21 trillion, with average APRs over 22%. Auto loans stretch to seven years for one in five new vehicles. Nearly half of renters now spend more than 30% of their income on housing.

A stock market built on sand

You’d expect Wall Street to slump alongside Main Street. Instead, the S&P 500 posts records. Why? Because 10 mega-cap tech stocks make up 40% of its total market cap. Strip them out, and the picture darkens.

More than 450 large companies filed for bankruptcy in the first half of 2025, the most since the Great Recession. Manufacturing has lost 78,000 jobs. Construction spending has fallen in seven of the past 11 months. Small caps fare even worse: 43% of Russell 2000 firms are unprofitable.

AI hype fuels the illusion. Nvidia’s data center revenue — half of it from just three shaky firms — drives much of the market. The S&P’s price-to-book ratio now tops the dot-com bubble. This is not sustainable growth; it’s speculation on steroids.

The housing bubble must pop

Housing has become the last pillar propping up the economy. Thanks to years of near-zero rates, federal subsidies, and trillions in mortgage-backed securities, the housing market ballooned to $55 trillion — $20 trillion more than in 2020.

But affordability is gone. The frozen market now shows cracks as prices fall in half the country. This is the moment to let it reset. Instead of lowering lending standards or declaring housing “emergencies,” the Trump administration should allow prices to match real wages.

Americans can’t keep using housing as a savings account or demanding 25% annual stock returns while complaining about inequality. You can’t have both free markets and endless asset bubbles.

RELATED: No peace without steel: Why our factories must roar again

Stop feeding the beast

Wall Street already salivates over another round of stimulus to keep the AI bubble inflated. Evercore ISI predicts the S&P could hit 9,000 by 2026, even while warning this could become the “biggest bubble ever.” By then, the economy would be addicted to corporate welfare, and taxpayers would foot the bill for the richest companies in history.

Enough. A nation cannot live on financial tricks and asset bubbles forever. Let the recession come. Let the bubbles burst. Only then can America rebuild a market economy rooted in work, savings, and production — not in debt and fantasy.

Won’t somebody finally stand up and shout stop?

Cracker Barrel's stock sinks after controversial 'woke rebrand'

Cracker Barrel Old Country Store made headlines this week after it unveiled a drastic rebrand, though not for positive reasons.

The 55-year-old chain replaced its iconic logo, which featured a man leaning against a barrel, with a more generic design that includes only the company's name.

'"Rebrand" all of that to something more modern, something more inclusive, and something that erases those feelings, and you're "rebranding" the SOLE reason why anyone goes there to begin with.'

The logo change comes after Cracker Barrel started changing its restaurant interiors last year. The updated look replaces the classic country style with a more modern design.

The update went viral online for all the wrong reasons, with many accusing the restaurant of going "woke."

"In college, I worked at @CrackerBarrel in Tallahassee. I even gave my life to Christ in their parking lot," Rep. Byron Donalds (R-Fla.) wrote in a post on social media. "Their logo was iconic and their unique restaurants were a fixture of American culture. No one asked for this woke rebrand. It's time to Make Cracker Barrel Great Again."

RELATED: Cracker Barrel ditches Americana as customers call for boycott over iconic brand change

Even Steak 'n Shake took a swipe at Cracker Barrel on social media.

"Sometimes, people want to change things just to put their own personality on things. At CB, their goal is to just delete the personality altogether. Hence, the elimination of the 'old-timer' from the signage. Heritage is what got Cracker Barrel this far, and now the CEO wants to just scrape it all away," the hamburger food chain wrote.

Though the company reportedly hired three marketing agencies to help with its redesign as part of a $700 million larger transformation plan, the public pushback appeared to negatively impact Cracker Barrel's stock.

Its shares fell nearly 15% during Thursday trading, dropping the restaurant's market value by $194.6 million, CBS News reported. Cracker Barrel regained some ground in the afternoon, with shares down roughly 13.9%.

"Shareholders should be absolutely infuriated," conservative commentator Robby Starbuck stated.

"Bottom line: Wokeness destroys businesses."

He called for Cracker Barrel's CEO to be fired.

Blaze Media co-founder Glenn Beck said, "Cracker Barrel CEO Julie Felss Masino said on Good Morning America this week that people are thrilled about the [restaurant's] rebrand. I think she's lying."

"Woke ideology has changed our country in countless ways, some of which we may never get back. But Cracker Barrel has always represented the one thing I think so many Americans currently crave: NOSTALGIA," Beck continued. "You go to Cracker Barrel for the rocking chairs outside, the meals that taste like grandma's home cooking, and the simple game of Chinese checkers on the table."

"'Rebrand' all of that to something more modern, something more inclusive, and something that erases those feelings, and you're 'rebranding' the SOLE reason why anyone goes there to begin with," Beck added.

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Private equity’s losing streak is coming for your 401(k)

One of the late comedian George Carlin’s most famous rants gave us the line, "It's a big club ... and you ain't in it.” That sentiment rings especially true when it comes to the financial services industry, where wealthy investors and insiders gatekeep the most lucrative opportunities for themselves and their friends.

So what should you think when they suddenly want to let you in?

The private equity party is a bit dim right now, and that’s why they are sending out more invitations. Be careful before you RSVP.

There's no red flag bigger than when someone wants to let you in on something very exclusive — especially if it’s from people who’ve spent decades keeping you out of the club.

Case in point: the private equity industry’s latest push to open its funds to everyday retail investors.

The private equity world is one I know well, as a recovering investment banker who works with a firm to evaluate deals. My husband also worked in the sector. Like any other industry, it has both good and bad players.

Private equity involves deploying capital to buy ownership stakes in private companies, distinct from equity invested through the public markets in publicly traded companies. These firms are often actively involved with the company, as opposed to the more passive investing in public market companies. Their stakes are typically substantial, often including majority ownership.

The good players in private equity provide capital, professionalization of businesses, governance, business insights, and capital for growth. They may reward employees with an ownership stake to align incentives.

Some private equity players, however, focus on financialization — that is, playing around with the capital structure of a company and not adding a lot of value otherwise. Private equity is rife with examples of firms that have ruined businesses with too much leverage and engaged in a variety of greedy — and often, outright abhorrent — behaviors.

But this latest trend isn’t about good firms versus bad firms. It’s about the broader industry’s poor performance — and desperation.

The returns are drying up

Private equity has a problem. Too much money has flooded the space in recent years, driving up valuations and pushing down returns. Funds are struggling to find new investors to cover their high management fees. So now they’re turning to you.

They aren’t suddenly being generous. They’re just trying to survive.

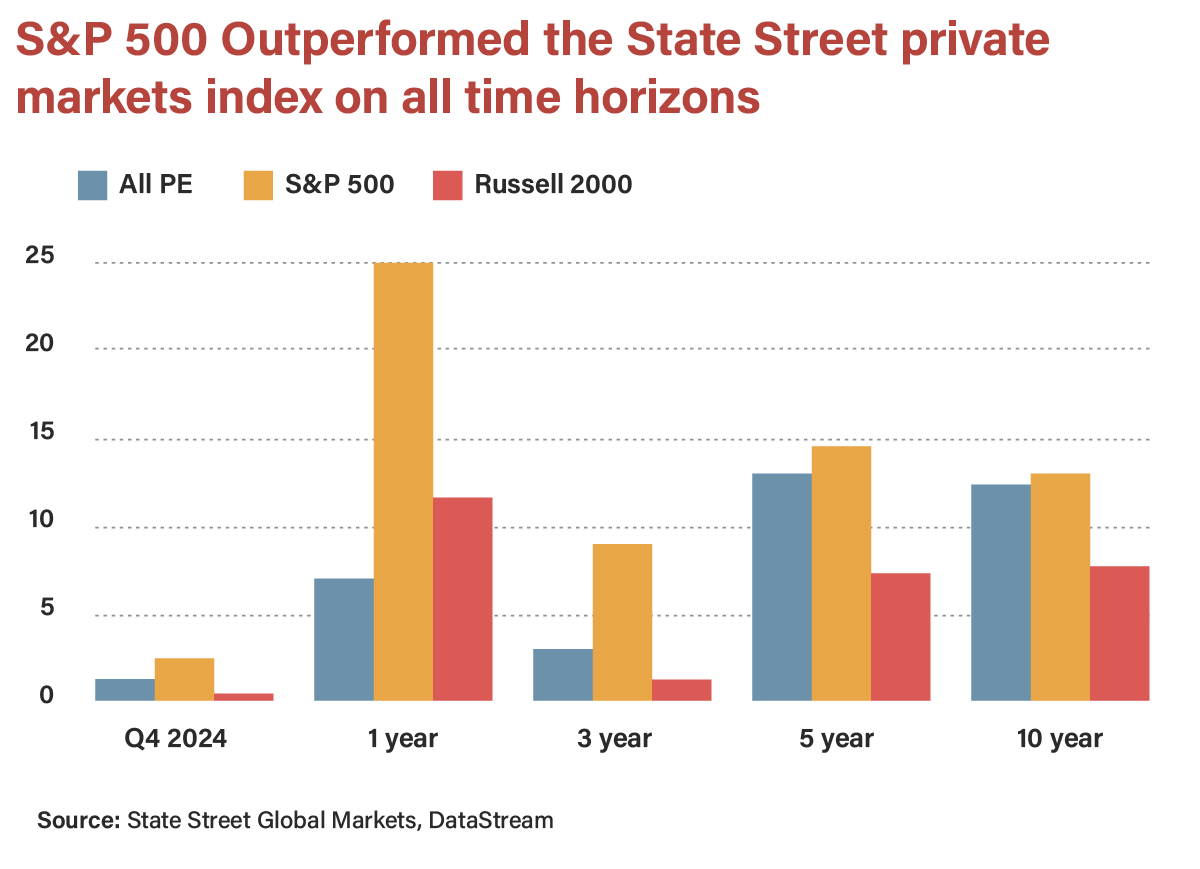

According to the Financial Times, a major private market index has underperformed the S&P 500 over the past one-, three-, five-, and 10-year periods. Any outperformance was skewed toward earlier years — and even then, it came with significantly higher fees and far less liquidity.

This underperformance comes with heavy fees and a lack of liquidity for your investment. It's not a coincidence that you are seeing private equity opening up to retail now when it is struggling from deal competition, higher valuations, higher capital costs, and slower deal exits.

RELATED: Red states get it: Economic freedom beats blue-state gimmicks

Speaking of slower exits, the Wall Street Journal noted that “private equity remains the biggest fee generator for the broader Wall Street ecosystem of banks and advisers” and that private equity firms are sitting on a record number of companies that they are waiting to exit — that is, sell and record a profit ... or a loss. Longer hold times for private equity firms mean they are not returning capital to their investors, and, in turn, the investors are not reinvesting in the latest and greatest fund.

Whether it’s the new push to allow private investments into your 401(k) or your financial planner calling you with “new, exciting alternative investment opportunities,” please be appropriately skeptical. Always probe a fund’s track record (especially over the past several years), fee structure, and whether it is a fit for your objectives and goals.

The private equity party is a bit dim right now, and that’s why they are sending out more invitations. Be careful before you RSVP.

S&P 500 hits new record high following months of Trump tariff doom and gloom

Just weeks into President Donald Trump's second term, the S&P 500 — which had risen over 20% in the previous two years — rocketed to record highs, driven up in part by a substantive increase in corporate earnings as well as the "Trump bump."

After marking its all-time high of 6,144.15 on Feb. 19, the index soon began to slide, prompting anxiety among some investors and doom-saying from various analysts, especially over the potential impact of the president's tariff proposals.

For instance, Andrew Brenner, head of international fixed income at National Alliance Securities, told the New York Times a month ahead of Trump's "Liberation Day" tariff announcements, "The tariff rhetoric has become daily and extreme, sentiment is awful and trading is on edge."

In the days immediately following Trump's April 2 announcements, the S&P 500 had its worst day since COVID-19 crashed the economy in 2020, then shed many trillions in market value, prompting more of the concerns and shirt-rending that would become customary over subsequent weeks.

After months of doom and gloom, the S&P 500 hit a new record on Friday, marking a stunning comeback from April. At market open, the S&P 500 went north of 6,154.79.

CNBC suggested that the comeback — what Bloomberg indicated is "shooting toward the second-biggest percentage-point recovery in history" — was driven in part by strong corporate earnings, a stable labor market, and new energy in the AI trade. It certainly doesn't hurt that trepidation over tariffs has largely given way to optimism over Trump's trade deals.

The possibility that Trump might not ultimately implement his Liberation Day tariffs may also have been factored into investors' optimism. After all, the rise came on the heels of White House press secretary Karoline Leavitt noting that Trump's July tariff deal deadline "is not critical" and "could be extended."

There's also the matter of Commerce Secretary Howard Lutnick's recent revelations to Bloomberg News that the U.S. and China finalized its trade deal this week and that the Trump administration has imminent plans to reach trade deals with 10 other major trading partners.

"We're going to do top 10 deals, put them in the right category, and then these other countries will fit behind," said Lutnick.

RELATED: Trump’s tariffs take a flamethrower to the free trade lie

"The markets are looking forward, seeing lower interest rates, less regulation in the banking sector, a shift from austerity to stimulus in Europe, and a less biting inflation and tariff environment," Jamie Cox, managing partner at Harris Financial Group, told CNBC. "This sure isn’t the stagflation story we've been told to brace for."

Paul Stanley, chief investment officer at Granite Bay Wealth Management, said to CNN regarding the S&P 500's $9.8 trillion roundtrip, "The market is betting on continued progress on trade and a de-escalation of tensions in the Middle East is giving investors confidence."

Entrepreneur and business expert Carol Roth told Blaze News that "it's important to remember that the market is not the economy, and that other factors, including the Federal Reserve and government policy, have impacted the market, particularly over the last couple of decades."

"The president's heavy-handed approach to tariffs was not expected by the market, but as there had been more certainty gained regarding tariff policy and a belief that further de-escalation is more likely than escalation, the market has moved past that hurdle," explained Roth. "In recent days, commentary from Fed members that suggests a Fed rate cut may be on the table for July has supported risk assets."

Roth noted, however, that "any long-tail effects from tariffs that show up later in the year, or challenges that arise from financing/refinancing our massive debt and deficit could shift the outlook and impact market returns."

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Exclusive: Republicans relish Trump's 100-day winning streak: 'We have momentum building'

President Donald Trump is officially 100 days into his second term, and many of his allies have celebrated the milestone as a roaring success.

Despite criticism from his political and media adversaries, Trump takes pride in his 100-day sprint, and Republican lawmakers are riding the momentum.

'He took the bull by the horns.'

"Well, I think either we've done everything, or it's in the process of being done," Trump told reporters Tuesday.

House Republicans are messaging in lockstep with the administration, sharing the president's enthusiasm in exclusive interviews with Blaze News.

"The first 100 days of President Trump can be summed up in one slogan: promises made and promises kept," Republican Rep. Ralph Norman of South Carolina told Blaze News. "It’s like a veil has been lifted from this country.”

"I think it’s been the best presidency that I’ve seen in my lifetime," Republican Rep. Eric Burlison of Missouri told Blaze News. "We’ve had four years to kind of plan and strategize what he would do when he returns, and we’re seeing the fruits of that."

One frequently referenced victory has been the southern border, which has seen record-low encounters with illegal aliens under the Trump administration. Between the inauguration and April 1, only nine illegal aliens were released back into the country, compared to the 184,000 illegal aliens released under former President Joe Biden during the same time frame last year, according to press secretary Karoline Leavitt.

'President Trump is fulfilling his promises, but the accomplishment to me is the rate he’s doing it.'

“The border security is incredible," Republican Rep. Marjorie Taylor Greene of Georgia told Blaze News. "It’s historic. And we have a lot of thanks that goes to President Trump, as well as Tom Homan."

“To do that in these first 100 days has been absolutely phenomenal," Republican Rep. Mark Harris of North Carolina told Blaze News. “He took the bull by the horns."

The numbers paint a very clear, indisputable picture on immigration. However, other areas like the economy have been swirling with controversy in recent weeks with ongoing trade wars and market uncertainty. Many critics, particularly in the media, have rushed to call the economy a failure. Despite their doom and gloom, the Trump administration and his supporters on the Hill remain confident.

'We have a long way to go, but he’s only been in office 100 days.'

"We were losing billions and billions of dollars a day with trade, and now I have that down to a very low level, and soon we're going to be making a lot of money," Trump told reporters Tuesday.

The consensus among Republicans was that Trump's presidency was not only a success but also impressively efficient.

"President Trump is fulfilling his promises, but the accomplishment to me is the rate he’s doing it," Republican Rep. Mary Miller of Illinois told Blaze News. "He was working on his transition team before he was even elected so he could hit the ground running, and that's what he’s done."

"He came in with the best Cabinet that I think we’ve ever seen," Burlison added. "He came in, and he got them appointed quickly, and he came in with a ton of executive orders."

While Republicans enjoy the successes of the first 100 days, lawmakers are tasked with maintaining the winning streak. The House and Senate are officially back in session after a two-week recess, and reconciliation talks are resuming.

“We have a long way to go, but he’s only been in office 100 days," Norman told Blaze News.

"I’m very excited about it," Miller said. "I think we have momentum building to pass this one big, beautiful bill."

While lawmakers in the House and Senate continue to iron out reconciliation talks, Republicans have maintained that Trump policies, such as no tax on tips, are a non-negotiable.

'Congress is not on page with President Trump, and I think that's a serious problem.'

“No tax on tips, no tax on overtime, and no tax on social security," Greene told Blaze News. "These were President Trump’s campaign promises that he said over and over again, promising the American people, and these are the promises that Congress has to deliver.”

Spending cuts have also remained a top priority despite the negative press from the legacy media surrounding Elon Musk and DOGE's efforts.

"It’s not going to be easy, but it’s like the cancer patient who’s taking the medicine that’s bitter," Norman told Blaze News. "I’m sorry, but if it will help you and cure the cancer, then we do it. And the cancer in this country has been overspending, and we’re going to fix it.”

"We’re at $37 trillion in debt," Burlison added. "We have a $2-trillion-a-year annual deficit. If we grow that, I can’t live with myself."

'We’ve gotta make sure we do government differently.'

Although some Republicans say we are on track, others are not confident that Congress will stay on course.

"Congress is not on page with President Trump, and I think that's a serious problem," Greene told Blaze News.

“If Congress does not deliver on these important campaign promises of President Trump, we’re gonna lose the midterms," Greene added. “It would be such a failure of a Republican-controlled Congress not to deliver on the mandate, the historic mandate, that was given in November.”

Although there are some concerns that Congress will return to old spending habits, Trump remains optimistic about reconciliation.

"If we get that done, that's the biggest thing. ... And I think we're going to get it done," Trump told reporters Tuesday. "We have great Republican support."

"We’ve gotta make sure we do government differently," Harris said. “We’ve gotta stay the course that we’ve started.”

Like Blaze News? Bypass the censors, sign up for our newsletters, and get stories like this direct to your inbox. Sign up here!

Exclusive: Report Shows Network News’ Maximum Slant On Trump Tariffs

A NewsBusters review shows ABC, CBS, and NBC devoted 62 times more coverage to Trump tariffs and market declines than booming jobs numbers.

A NewsBusters review shows ABC, CBS, and NBC devoted 62 times more coverage to Trump tariffs and market declines than booming jobs numbers.