The Fed’s independence has become a constitutional absurdity

The independence of the Federal Reserve System has become a major source of public controversy. As political leaders signal dissatisfaction with monetary policy, officials and commentators rush to defend the central bank’s insulation from democratic pressure. We are told, as if it were self-evident, that central bank independence is a pillar of sound economic governance.

But this confidence is misplaced. The economic case for central bank independence is far weaker than its defenders suggest. And the constitutional case is weaker still.

Officials entrusted with such consequential authority must ultimately answer to elected leadership.

Start with economics. The standard argument is that independent central banks deliver low and stable inflation because they are insulated from short-term political incentives. Elected officials, facing electoral pressures, might be tempted to juice the economy with artificially loose monetary policy. By contrast, independent technocrats can take the long view.

Early empirical studies did show that countries with independent central banks experienced lower inflation. Yet more recent research has cast doubt on this relationship. The correlation is sensitive to different samples and methods. In many cases, the supposed benefits of independence disappear entirely.

A more plausible explanation has emerged. Countries that enjoy low and stable inflation share deeper institutional characteristics: respect for the rule of law, stable political systems, and credible commitments to property rights. These are the real foundations of sound money. Central bank independence accompanies these basic governance norms, but its stand-alone effect is debatable.

This matters for a free-enterprise economy. Monetary policy is not a neutral technocratic exercise. Interest rates are prices: the price of time, risk, and capital. When insulated officials tinker with those prices at their discretion, the result is distorted market signals. Cheap credit can mislead investors, encourage unsustainable projects, and redistribute wealth in opaque ways. Independence does not eliminate politics. It simply hides politics behind a veil of expertise.

If the economic case for independence is overstated, the constitutional case is entirely bunk. The Constitution is clear: Congress holds the power “to coin Money” and “regulate the Value thereof.” Monetary authority, like all legislative power, originates with the people’s representatives. Congress may delegate certain functions to administrative bodies, including by creating a central bank. But delegation is not abdication.

Those who exercise delegated authority remain accountable to the laws Congress passes and, ultimately, to the chief executive charged with enforcing them.

Yet the modern Fed operates as if our constitutional framework were irrelevant. Its leaders enjoy significant protection from removal. Its decisions (targeting interest rates, allocating credit, regulating banks, etc.) have sweeping consequences for the entire economy. If this does not constitute the exercise of executive power, it is hard to say what does.

The Supreme Court has recently emphasized that administrative agencies cannot be insulated from presidential oversight simply because they possess technical expertise. The separation of powers does not yield to convenience, nor to the promise of better policy outcomes. Yet when it comes to the Federal Reserve, the court has signaled a willingness to tolerate precisely such insulation — a “special case” for the most powerful economic institution in the country.

This exception is indefensible. Appeals to history or prudence, however well grounded, are not constitutional arguments. An agency that wields executive power must answer to the chief executive. Concerns about how that works in practice does not justify ignoring the Constitution.

The truth is that central bank independence persists not because it is firmly grounded in law or economics, but because the alternative unsettles us. We worry, not without reason, that elected officials might misuse monetary policy for short-term gain.

But the Constitution does not permit us to resolve that fear by concentrating vast economic power in the hands of unaccountable experts. A free and self-governing people must confront the difficult task of designing institutions that combine competence with accountability.

RELATED: If Congress can’t oversee the FBI, who can?

That begins with Congress. There are several legislative reforms that can restore the rule of law to monetary policy. First, lawmakers should narrow the Federal Reserve’s mandate to a single, clear objective — price stability — rather than the vague and conflicting goals it currently pursues. A simpler mandate would make it easier to evaluate performance and hold policymakers responsible when they fail.

Second, Congress should revisit the legal protections that shield senior Fed officials from removal. Freedom of judgment is one thing; freedom from oversight is another. Officials entrusted with such consequential authority must ultimately answer to elected leadership. Legislators ought to make it easier to fire central bankers.

Finally, the president should take a more active role in ensuring that the Fed operates within its statutory and constitutional bounds. This does not mean dictating day-to-day interest rate decisions. Instead, it means recognizing that monetary policy, like all exercises of government power, must remain subject to democratic control.

President Trump’s nomination of Kevin Warsh as the next Fed chairman is a good start. The two must work together to restore the Fed’s ordinary day-to-day operations, something missing since the 2007-08 financial crisis.

Economic stability is obviously desirable. But we cannot purchase it at the cost of self-government. Republican principles require officials to be answerable to the people. If we are serious about preserving the constitutional order and free enterprise, we must abandon the comforting myths of central bank independence and restore accountability to the Federal Reserve.

Editor’s note: This article appeared originally at the American Mind.

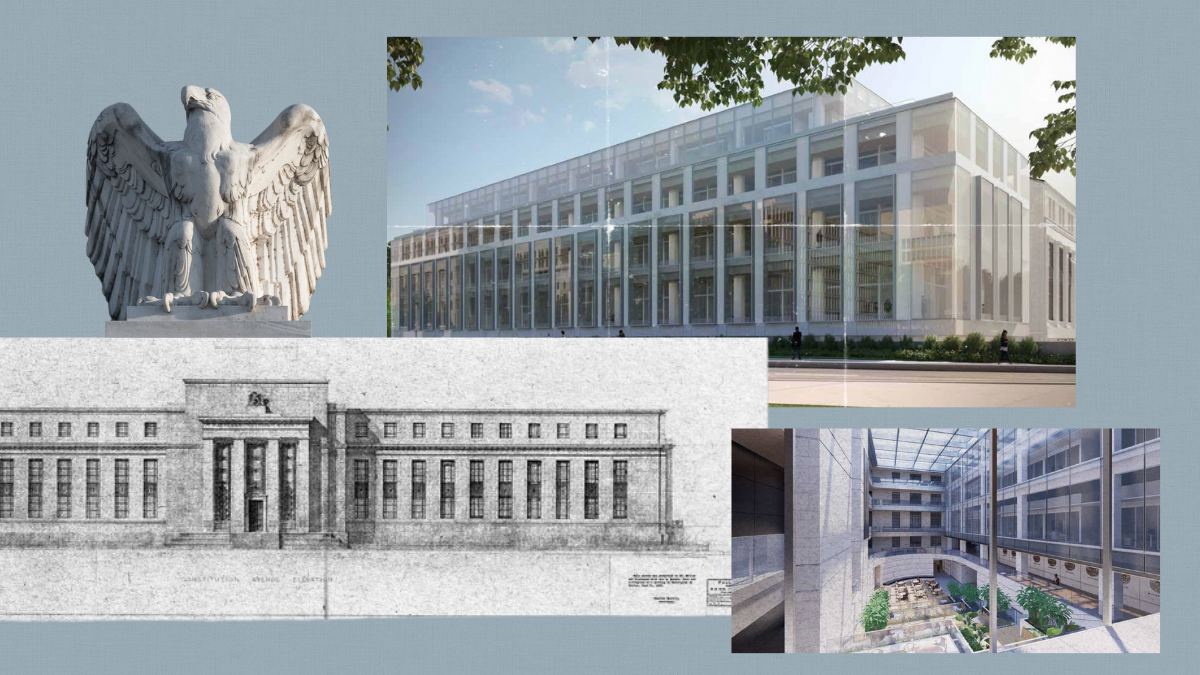

If we're going to build palaces for our bureaucrats, can they at least be pretty?

If we're going to build palaces for our bureaucrats, can they at least be pretty? The decision marks a turning point for the administrative state and the end of an era for self-funding, self-governing agencies.

The decision marks a turning point for the administrative state and the end of an era for self-funding, self-governing agencies.

Photo by Chip Somodevilla / Staff via Getty Images

Photo by Chip Somodevilla / Staff via Getty Images

Photo by e-crow via Getty Images

Photo by e-crow via Getty Images

Photo by Win McNamee/Getty Images

Photo by Win McNamee/Getty Images Photo by Chip Somodevilla/Getty Images

Photo by Chip Somodevilla/Getty Images

It's highly unlikely that the solution to a problem caused in part by poor Federal Reserve policy can come via yet another policy intervention by Fed officials.

It's highly unlikely that the solution to a problem caused in part by poor Federal Reserve policy can come via yet another policy intervention by Fed officials.